但是我看了一些人,作为一个丈夫的妻子,或者作为一个妻子的丈夫

彼此写给对方的信件,短文

以及作为孩子的母亲,作为孩子的父亲

彼此写给对方的信件,短文

我又觉得,这句话说得不对

比如很多人在八卦中,写张爱玲出卖家人,但是我看过张爱玲的散文短文,她写自己生活的情绪不是极端的也不是灰暗的

以及我看林徽因写给自己家人孩子的信件,也不是那种调调

ps.父母写给孩子的信,夫妻彼此写给对方的信,如果没有恨意,就不是卖淫

我对这个姓沈的父亲的印象,起始于我读幼儿园大班。在更早的时候,我没有任何关于父亲的印象

关于母亲的印象也没有,就算有印象,也是这个姓傅的母亲,无时无刻不断灌输给我的

幼儿园大班,我唯一的印象,就是姓沈的父亲,每天接送我去幼儿园上课,或者是姓傅的母亲每天接送我去幼儿园上课

到了小学,我唯一的印象就是姓沈的父亲出差,姓傅的母亲总是不在家http://ytilauxes.blogspot.com/2016/08/dear-translator.html,而我住在5楼或6楼,总是停水,我会在家里空无一人的前提下,在不停水的时候,把家里的水盆接满水

小学的冬天,就连下大雪,雪积得很厚很厚,都是我自己,一步一个脚印,走到学校去

小学的2个学年,因为家里没有人,我连放学也不回家,而是每天放学后在外面玩,直到把书包玩丢了我再回家

从幼儿园大班,到小学2年纪结束,前后3,4年,印象中就是我一个人渡过的,或者还有同学的陪伴

我没有跟家人比如跟父母在一起的生活经历的印象,连在一个饭桌上,三人一起吃早饭,晚饭的印象也没有http://ytilauxes.blogspot.com/2016/08/dear-translator.html

后来就是我到上海来了一次,再后来我定居在上海

我也没有任何的印象,跟父母在一起,连在一张饭桌上吃饭的印象都没有

我父母离异的时候,我全程都没有参与,但法官问我你跟爸爸在一起生活,还是跟妈妈在一起生活,我说我跟妈妈在一起生活

我爸爸带走了大多数的物品和钱,留给我和妈妈一部分,只属于我们两个人才能用的物品,从此,我爸爸再也没有来看望过我

小学毕业,我就整天读书,考试成绩最好

我爸爸有时会故意叫我去他再婚家庭的住处,拿生活费,并要求我在生活费的本子上,签字,以表示,这个月,把生活费给我了

之前还是我爸爸主动把钱给我妈妈,后来我爸爸每次都要求我去拿生活费,每个月我都要签一次名

我爸爸把他再婚儿子和再婚老婆吃剩下的零食,带到我的学校,交给我初中的班主任,我初中的班主任把这些食物交给我,顺便大骂我爸爸,骂了足足一个多小时

后来我再也不跟我爸爸打交道

我爸爸再婚对象是个文化人,画画,看书,自己学裁剪,做衣服

我爸爸再婚以后又觉得跟她没有共同语言,而觉得我妈妈好,所以多次要求跟我妈妈复婚(我妈妈也是看书,自己做衣服,织毛衣,唱歌跳舞,跟那个再婚妻子的性格很像)

但是我妈妈也没有搭理我爸爸

我爸爸后来头发一夜之间变白,我妈妈单位的人看到我爸爸,认为那是我妈妈的父亲

我妈妈离婚后很年轻

但后来也变得很难看,比如身材不好,皮肤变差

我跟我爸爸偶尔的几次接触,都是跟他再婚的妻子,再婚妻子的亲生儿子,在一起接触

我爸爸再婚妻子的亲生儿子,出了大事,我爸爸拿钱,带人,去给他再婚妻子的亲生儿子冒犯的他人,赔礼道歉,赔钱,以及带对方去医院看病

我自己生病,却也没有住过院,我爸爸从来不陪我去医院看病

我另外见到的跟我爸爸有关的人,是我爸爸再婚又离异之后的同居对象,她话很少,送我一件很难看的毛衣

后来这个同居对象的女儿,生了孩子,我爸爸替这个同居对象的女儿所生下来的孩子,带孩子,以及给这个同居对象,及女儿女婿和他们生的孩子,做一日三餐的饭

但是我不记得我爸爸做过什么饭菜给我吃

我只记得,当我爸爸要求我去见,他的再婚对象,再婚对象的孩子,他的同居对象,他会做菜给我吃

以前他做菜放很多盐,后来炒菜却不咸了

儿时的照片,都不是我爸爸给我拍的,而是爱好摄影的舅舅,在舅舅给自己家人拍照时,我的舅舅会给,寄养在外婆家的我,拍几张照片

我爸爸买过不止10只照相机,但是我爸爸一点都不喜欢摄影,也从来不给我拍照片

我姨夫喜欢摄影,我姨夫的儿子,从小到大,每个成长阶段的样子,我姨夫都用镜头记录下来

我却不知道自己小时候长成什么样

我爸爸五音不全,学唱歌,也不能够把一首歌,从头到尾唱一遍

我却在初中参加合唱队,唱高音,领唱

我曾经见过些许我爸爸年轻时的照片,他比较纤瘦,个头却不高,皮肤特别好,到了今天,他几近70岁,却脸部也看不出有皱纹的样子

我妈妈的皮肤不是我爸爸那样,我自己皮肤也不是我爸爸那样

我爸爸有一些照片皮肤晒得很黑,像是晒过日光浴的样子,我爸爸本人真实的样子,其实是皮肤很白

我爸爸写字,字体让人难以辨认,我写出来的字,却是字形比较大气,我没有练过一分钟书法

我跟我爸爸的性格不太一样,我爸爸也很少跟我交流,但是我觉得我爸爸记忆力似乎很好,比如我经常发现,别人让他在我面前说些什么话题,他都能够从头到尾把这些话题,很顺利的背一遍给我听

我爸爸性格内向,我妈妈我去问她你性格外向吗,我妈妈说自己性格内向,我在同学面前性格外向,其实性格也是内向,这是我们家三个人共同的特点

而我妈妈家族,外公傅姓,外婆林姓,外公外婆的子女,子女的子女,都是内向型性格

我爸爸最大的特点就是用情专一

但是他有过三段感情生活,然而他跟谁在一起共同生活天天见面,除了在第二段感情时,想过跟我妈妈复婚以外,后来他跟别人在一起,就再也不会想到其他人,而把这个眼前跟他一起生活的人

的一切,看作是自己的一切

所以他就忘了我是他女儿

而我对于妈妈的印象,就是她终日歇斯底里

后来我看了一本书的简介,是弗洛伊德写的,他在书中表达的意图,女性,没有定期的性生活,就会有歇斯底里症

我妈妈跟我爸爸离异后,我妈妈跟我前继父同居

从此,我再也见不到我妈妈歇斯底里

但是我前继父却跟我吵架,我妈妈又对我歇斯底里,帮着我前继父,一起骂我

我妈妈和前继父08年离婚,是我要求的,离婚以后,我妈妈又整天歇斯底里大骂我

其实我在06年曾写博客提及,我要替我妈妈买一套大房子

但是后来我看到郎咸平写的房地产文章,就招致我自己被强奸

我妈妈替强奸我的人,连续多年来,不间断的辱骂并殴打我,而且不给我饭吃

我妈妈跟前继父在一起,就是吃,玩,跳舞,旅游,唱歌,她说自己是内向性格,我却觉得她见到谁都很开心,典型的外向性格

我妈妈性欲旺盛,但是我自从交往了恶狼恶狗王菲,跟他在一起没有性欲以后,有人给我妈妈吃药,她连身材都变了,本来她的身材是,腹部平坦没有赘肉,后来她整个腹部都凸出来,并整天说自己,觉得性很恶心,然后又因为离婚,冲着我歇斯底里

我外公也知道我妈妈歇斯底里,也知道我妈妈跟前继父在一起不歇斯底里,所以我让我妈妈跟前继父离异,我外公就骂我,说,征得我同意的前提下,让我前继父跟我妈妈复婚

我妈妈跟前继父在一起

买了不少物品,我前继父是个喜欢穿衣打扮的男人

跟我爸爸在一起时,我妈妈看起来质朴,跟前继父在一起,看起来风尘

我前继父交往的各种女人,我妈妈都认识,并且跟对方吵架,打骂

所以我妈妈在我心目中的印象,很不堪

因为这个不堪的妈妈的印象深入骨髓,所以只要我表现出一点对她的反感,我妈妈就给我猛灌各种药,这样,我妈妈各种不堪的事迹,我就丝毫回忆不起来

我还想起,06年我在6.4纪念日前后,在看万科集团的官方论坛,而06年的6.4前后,我妈妈在西安的亲戚,全都拍了一组,拜佛的照片,佛教对于这些人的寓意,就是,纵欲,斗争,屠杀http://capitalismchina.blogspot.de/

最近我自己主动说,我曾经抱怨过姚宁不给我买东西,我妈妈就主动告诉我,她跟我爸爸结婚,拍了一组照片,她很忧郁的样子,也是因为,我爸爸在跟我妈妈结婚时,我爸爸,我妈妈的母亲我外婆,不给我妈妈买东西

6.4前后,我还发现一个在法国ELLE杂志任职的女人,晓雪,是万科集团王石的二奶

后来因为有人给我吃药,我在6.4前后行为失控,我就在万科集团的论坛上,注册了id,并把万科王石的二奶,晓雪等事迹,写在万科集团论坛上

后来万科集团就突然出现无数条,律师的发帖,涉及离婚夫妻财产分割等

还说起,作为丈夫的妻子,喜欢奢侈品是个什么态度。万科王石的二奶,晓雪,就终日使用奢侈品

万科集团的论坛后来改版了,上面的帖子,至少是06年的帖子,都没有了

我还产生幻觉,以为我要去万科工作,还写帖子,或者是写在自己博客或者就是计算机的记事本上,说是去万科工作,应该要给我股权

但是后来我就再也没有关注过跟万科有关的任何事项。有一天我砸了商场的柜台,被警察带到警察局前,我说起中国那么腐败为什么还要坚持这个体制,以及我说房地产价格那么高为什么还要坚持

警察就把我抓起来,后来我还说温家宝要把万科股份送给我,我说我不要,警察就说,给你,你为什么不要

强奸我的不知是什么人,但是跟我在万科集团论坛发帖有关,也跟我谈及各种政治问题有关,也跟我说起郎咸平谈及房地产话题有关

我妈妈后来又多次拍摄拜佛的照片,佛教对于这些人的寓意,就是,纵欲,斗争,屠杀http://capitalismchina.blogspot.de/ 所以其实从我对家人有记忆以来,85年86年的样子,我的其他家人,尤其我妈妈,终日的表现,就是恶狠狠的斗争。我妈妈说任何话题,涉及整个社会任何阶层的人,都是恶狠狠的,连说起自己两任丈夫,也都是恶狠狠的。

在我妈眼里,男人就是做鸭畜生,女人都是鸡

我妈说男人都是畜生做鸭,女人都是鸡,而我如果表现出觉得我妈不堪,我妈就给我吃药,让我得遗忘症。我妈还恶狠狠说,因为我觉得我妈不堪,所以我活该被强奸受到惩罚,强奸我的人是徐静蕾派系citic中信王震家族等人,因为citic中信王震家族在06年就让徐静蕾找人代笔写博客,说法律如何如何,我妈就替徐静蕾和citic中信王震家族,整天辱骂并打骂我。徐静蕾的其中一任男友,听暗黑音乐http://ytilauxes.blogspot.co.uk/2016/07/all-dark-arts-have-their-own-will.html的张亚东,在06年也提及法律等话题。另外提及法律这个话题的是跟曾庆红朱镕基派系有关的,我认识的一个大唐电信的网友(是网易论坛主动搭理我的网友http://ytilauxes.blogspot.nl/2016/07/google163neteasekdnet.html),这个网友的网名是moodyblue,他曾亲口告诉我,自己喜欢去酒吧KTV,还在类似提供色情服务的足浴城和洗浴场消费过

我妈的经济状况也有所隐瞒

她在08年初的时候,也不过告诉我,自己公开的退休工资收入是1000余元

但是她有很多在各地旅游的照片,全都是她02年8月以来把1000元退休工资收入给我以后,她身边就只有我前继父给她的1000元家用的前提下,她外出进行的花费

这些钱哪儿来的,谁都不知道

因为从上海去外地旅游10几天,花费起码5000元以上,而这种外出旅游10几天的旅游,她从01年02年起,出去了不止5次

其余外出旅游5天以上的行程,从01年以来她也出去了10余次都不止

2016年8月31日星期三

2016年8月30日星期二

http://www.tianya.cn/27077215/bbs这个贴里提及我舅妈,说她跟人一夜情

http://www.tianya.cn/27077215/bbs 但是我回头再去看主贴,跟帖,楼主回帖,就又找不到其中提及我舅妈的回帖和跟帖了

我舅妈自己说,他父亲是崇明人,建国后在上海市区的一家,国营工厂工作

66年前后,工厂要搬迁到西安,我舅妈的父亲就自己一个人去了

他把自己的妻子,儿女,全都留在上海

后来我舅妈发现,自己的母亲,跟别的男人睡在一起,就写信把这件事告诉给她的远在西安的父亲

他父亲大怒,就下令他们全家,他的妻子儿女,全都到西安去生活

在我舅妈适合结婚的年纪

我舅妈的父亲看上了我舅舅,觉得我舅舅聪明,就让我舅舅娶我舅妈

我看到过不少我舅妈我舅舅,以及,我舅妈舅舅生的儿子,三人一起拍的照片

在文革年代,很多人挨批斗,生不如死,我舅舅却拍了一些照片,还有一张照片在北京拍的,拍摄年份是74年,以及后来76年前后认识我舅妈,77年左右结婚,78年生了我表哥

但是别人挨批斗,生不如死的时候,我舅舅没有参与到西安的文革运动中去,也没有斗过任何人

我妈妈家族,就是外公姓傅,外婆姓林,子女等,也算不上是文革逍遥派

因为我阿姨下乡了,得肝炎,我外婆弟弟的老婆干重体力活,热死了,我妈妈上海的亲戚,因为爱漂亮,烫头发,穿小裤脚管长裤,被剪了头发,被剪了裤子,以及上海的亲戚,下乡后跟知青生了孩子,男知青后来被车撞死了,我妈妈亲戚自己带大孩子

还有什么事情,我妈妈还没跟我说过,比如有亲戚在百胜集团工作或者在可口可乐工作,但工作的职位是很艰辛的那种

我妈妈家族,外公外婆,及子女配偶和儿女,就只有这个舅妈,为人处事比较行

但也不是社会上八面玲珑的女强人类型,也不是另一种,擅长散发女人味的那种人

我舅舅也不知是什么原因,事业心不强,跟他一起从事会计职业的同事,都去考职业资格证书,我舅舅却考不过,连会计上岗证都没有

我舅舅舅妈的爱好不太一样

我舅舅喜欢无线电,喜欢摄影,喜欢电器

我舅妈喜欢各种有意思的东西,吃穿用她什么都喜欢

我舅妈喜欢这些,也说明她家庭背景很一般,没什么家底,如果有家底的,家里祖传留下很多好东西,就不会觉得,外面卖什么,她喜欢什么

所以我舅妈舅舅的矛盾就在这里

我舅舅有了钱,就想存起来,他存钱什么意图我也不知道,可能是应对孩子的成长,买各种学习用具,交学费

我舅舅确实给我表哥买了很多很多物品

我表哥有很多很多很多书,他现在很多很多很多书,扔掉了一大半都不止

过去流行连环画,我舅舅给我表哥就买了各种名著的连环画

后来我舅舅又给我表哥买录像带,他们把好看的电视全录下来,我舅舅还喜欢看越剧,也都录下来,录像带录装满了几个抽屉

我舅舅还在流行小霸王学习机时,买给我表哥,以及买各种其他比如游戏机给我表哥

我舅妈具有小资品味,她自己姿色也上乘,所以她最大的遗憾是,没有生一个女儿,这样就可以既打扮自己又打扮女儿

我记得我小时候,我舅妈就打扮我,不过我小时候不好看,很快就长胖了,越打扮越难看

儿时我经常跟我表哥吵架,甚至打架,我跟我表哥在暑假寒假都跟外婆一起渡过

我跟我表哥打架,我舅舅舅妈不会打骂我,但我阿姨会去打骂我表哥,所以我舅妈心疼儿子,就跟我阿姨吵架打架

我跟我表哥打架时,外公外婆在一边劝架,唯独我阿姨会去打骂我表哥。我阿姨现在看到我表哥儿子,像看到杀全家凶手一样,看到我表哥,也像是看到杀父仇人一样

我阿姨跟我表哥从来不联系,我阿姨还仇视我表哥老婆,也跟我表哥老婆和表哥吵过架

我阿姨还跟我舅妈打架,却不是因为小孩的矛盾

我阿姨跟我舅妈两种性格的人

我舅妈看谁都顺眼,跟谁关系都好,喜欢交朋友,喜欢让朋友来家里做客,喜欢到朋友家做客

我阿姨几乎没有朋友,看谁都不顺眼

不过我阿姨姨夫关系很好,他们俩是天生的互补的一队

我也不知道我舅妈为什么跟舅舅离婚

但主要原因还是因为我舅妈出轨

就是很多人说的七年之痒之类的话题

我舅妈出轨以后,我舅妈舅舅离婚了,我舅舅和表哥住在一套1居半室的房子里,我舅妈住在2居室的房子里

后来工厂搬迁,我舅舅表哥住在2居室的房子,我舅妈住在2居室的房子

我舅妈舅舅互相之间也来往,并不是像仇人那样,彼此仇视且老死不相往来

但是我舅妈没有给过我表哥一分钱抚养费,也很少去看我表哥

我表哥很喜欢她妈妈,但是我舅妈不去看望他,我表哥也不会主动去看望自己妈妈

我表哥总是在,我妈妈,我,在西安,跟我舅妈联系的时候,再去看望自己的妈妈

我舅妈跟现在的丈夫一见钟情,闪婚

过到现在也有20多年了

但是我舅妈跟人相处的模式,让我难以理解

就是她在各种人面前,把自己丈夫说得一无是处,但是在家里却跟自己丈夫好得如胶似漆

如果仅仅凭借我舅妈对自己丈夫,不管是哪任的评价,来判断,她自己的婚姻生活是否和睦,其实很难搞清楚她到底过得好不好

我舅妈的性格和脾性,是属于玩性比较大的类型,但是中国自古有句古话,玩物丧志,她的表现虽然不是玩物丧志,但是她确实喜欢玩,她喜欢跟很多人聚在一起,作为聚会之中,众多人之中的焦点,她也喜欢邀请朋友来家里玩

我舅妈另一方面却也是个合格的妻子,她做家务很擅长,尤其擅长做饭,她的收入始终不高,这些收入不足以支撑她过那种,聚会焦点的日子,但她可以,靠自己节约,自己做饭,举办聚会,让自己过得有声有色

她做得一手好菜

我舅妈的丈夫,喜欢的是穿衣打扮,书画摄影,确实有些古语玩物丧志的样子,他还喜欢音乐会乐器弹奏

我舅妈跟自己丈夫在一起,就从过去喜欢穿衣打扮,到现在,省钱让丈夫穿衣打扮

这个丈夫把自己微薄的收入系数交给我舅妈打理,我舅妈再给他一笔零花钱,这个丈夫另外买衣服烟酒,钱是我舅妈出,所以如果任由这个丈夫花钱买烟酒穿衣,家里的钱很快会用完,但是我舅妈却会偷偷存一些钱,而告诉这个丈夫,家中存款其实不多

跟我舅舅在一起,我舅妈却是不存钱

我舅舅一直在工作,工厂破产以后也在工作,所以我舅舅工作之余,积攒了一笔工资收入,我舅舅另外还有奖金收入,直到09年我舅舅突然去世,我舅舅提及他要买房,而当时西安我外婆家小区附近的房价是4000余元一平方米,我舅舅说他不愿意跟外婆住在一起,而是要另外住一套房子,他说他准备买2居室房子,这大概有7,80平米

所以我不知道我舅舅究竟攒了多少钱

我舅妈工作的时候就是插拔电话线,不工作的时候也从来没工作过。

我舅妈的丈夫也没有工作过

但我舅妈的丈夫对外却说自己有个固定工作但其实他一直没工作,但是他不知哪儿来的收入支持他活下去,对外他说他有固定单位一直在单位工作且同事众多,电话本中都是同事的电话号码。

后来为了掩人耳目,我舅妈再婚丈夫和我舅妈,俩人做了一点小生意,就是自己花钱在新疆住了几个月,但钱哪儿来的谁都不知道,卖什么产品也没人知道。在新疆他们俩连天池都去过了,就是在新疆一直游山玩水

他们有很多游山玩水的照片,以前大量的照片贴在QQ相册,现在QQ相册照片全删除了

除去他们在新疆游山玩水几个月住在那里的花费

按照我开始关注他们俩的生活,他们一个月起码跟朋友聚会一次,就是,不是去朋友家,就是朋友来他们家,或是外出在饭店,跟朋友一起聚餐

除此,一个月至少外出旅行一次,旅行指的是离开家,至少在外面住3天以上

一年还要长途旅行至少一次,就是乘火车10几个小时那种

这样模式的生活,从97年98年搬到西安郊区就是如此。他们有大量游山玩水的照片,在数码相机发明以前,这些照片都是胶卷冲印,其中一些游山玩水的照片,跟我妈妈和她们一起聚会的重合,但跟我妈妈聚会的照片,只是很小一部分。后来有了数码相机,就每隔几天传到QQ相册,但最终她自己又删掉了QQ相册的所有照片

我舅妈喜欢成为人群中的焦点,而确实有很多男人围着她转,就连聚会拍照,那些男人都以,可以搂住她拍一张照片而感到喜悦

而我小时候记得,为了跟工厂司机搞好关系,她把工厂司机请到家里,司机脱光上衣,她就在拉上窗帘的阴暗的房间很暧昧的摸司机的背

她交往的司机的妻子叫陈来弟,文革期间的产物,父母希望生个儿子。这个司机五大三粗像混黑社会的,但那时还没有黑社会

我舅舅舅妈关系不好,表面是为了钱,其实是其他方面的问题,主要是我舅妈跟各种男人暧昧不清

但是离异以后他现在的丈夫不管这些事,我舅妈也当现在的丈夫面,提及陈来弟的五大三粗的司机丈夫

我表哥一直跟爷爷奶奶生活,也就是我外公外婆,我表哥的外婆外公全家根本就不喜欢他。后来离异了,我表哥就三餐吃在外公外婆家,没离异以前,三餐吃也吃在外公外婆家

所以我表哥是外公外婆带大的

但是我阿姨说,我表哥是个势利眼,我舅舅死了,外公外婆老了,我表哥就去亲近他妈妈,让他妈妈帮他做这个做那个

我阿姨仇视我表哥,仇视我表哥老婆,仇视我表哥儿子,就像是,他们三个,把阿姨全家上下,杀绝了一样

我表哥也同样仇视我阿姨

我外公外婆老了,最初外公外婆住院,表哥还帮帮忙,后来表哥就再也不管外公外婆了

我阿姨一直工作,最艰辛的工作,工厂倒闭后也是从事最艰辛的工作

但是我阿姨也莫名删除了很多QQ相册的照片,这说明很多年里,至少是5年间,她一直在玩

不知从什么时候起,可能是因为我在网上说了什么言论,引起什么人的警惕,我阿姨,我舅妈等人,包括我表哥,在一夜之间,全都把QQ相册里的,5年多前甚至更早的照片,删除得一张都不剩

我表哥最初在西安的工资不到1000元,这时就已经跟老婆结婚了,她老婆的生活水准,就是在反季节的时候买最贵的水果当饭吃,比如西安的芒果属于反季节水果,她就一天买2,30元芒果,芒果上市几天她吃几天

也不做饭,整天在外面吃饭

到处跟我舅妈一起出去聚会和旅游,不上班,没一分钱收入,买的东西却至少是外资的在国内合资品牌的档次

我妈妈说,她每个月花那么多钱,是我舅舅另外把自己工资和存款贴给她用

但实情是怎么回事,我却不知情

后来她又提出离婚,要求我舅舅支付彩礼,支付赡养费,分我舅舅的房产

我们都觉得这事跟我舅舅没关系

而是我表哥应该出面处理

最终婚没有离,财产没有分,我表哥老婆就病倒了

在病倒以前,他们生了一个孩子,而我舅舅在表哥老婆怀孕时,就死了

我表哥老婆对孩子非常狠毒,经常是恶狠狠毒打自己儿子,并大喊,打死你打死你打死你

但是没多久她就病倒了

我表哥的儿子就被接回了西安

跟自己妈妈我表哥老婆在一起时,我表哥儿子,站着拉屎

我表哥7,8岁的时候,我舅妈就再也不见他了

7,8岁以前,我表哥由外公外婆爸爸带大,我舅妈整天玩,跟各种女友好友在一起玩,还跟其他人在一起玩,比如五大三粗的司机

我表哥没有受到过正常的家庭教育,从小就不懂得自己整理衣物,自己整理书包,用过的东西也不知道自己放回去

所以后来我表哥结婚,跟老婆在一起,俩人喝牛奶,要把塑料袋剪一个三角出来,他们俩就在家里,各个角落,剪了无数个三角,在家的地板或桌上

我表哥老婆大概也是我表哥这样的人,所以表哥老婆有了儿子,就让儿子站着拉屎

我表哥的妈妈我舅妈,离开我表哥以后,跟自己新婚丈夫在一起玩

新婚丈夫有个儿子,但出生时被抱错了,等于这个新婚丈夫生了儿子以后,领到身边的是其他人的孩子

新婚丈夫没有养育过自己的,并不知情的“亲生”儿子

这个“亲生”儿子,由自己妻子抚养

新婚丈夫后来跟妻子离婚了,90年代就跟我舅妈结婚

所以我舅妈,和新婚丈夫,都不是爱孩子的成年人

他们俩的婚姻,在双方都没有孩子的负担下,过得很好,整天就是玩

我表哥有了孩子以后,没有麻烦自己亲妈,让她带孩子

而是我表哥自己跟老婆,201几年时,全都去了深圳,把孩子也带去了深圳

但后来他们出意外,表哥老婆病倒了,病倒以前表哥老婆对孩子也不好

最终就只有我表哥的妈妈,表哥妈妈新婚丈夫,俩人一起,带我表哥的孩子

我表哥的儿子,成长过程中

父亲,母亲,两个双亲的角色,缺位

所以表哥儿子的性格,为人处事,都有点问题

而我表哥的妈妈的新婚丈夫,可能非常嫉恨我表哥的妈妈

在我表哥儿子成长的每个点滴,哪怕学说话,以及学习跟长辈相处的过程中

都不断向我表哥儿子灌输各种奇怪的观点

我表哥儿子就变得越来越霸道,而且对奶奶,也就是我表哥的妈妈的态度,越来越不好

我亲眼见过这种情形

我认为小孩就是记性差,不记仇,但是大人在孩子面前灌输什么观点,日子久了,小孩就会形成什么观点,并对某些事情,做出条件反射般的回应

http://www.tianya.cn/27077215/bbs 这人发贴提到那么多事情,

比如天涯网站有个ID sophgold 还有个ID 克莱因瓶里的猫

以及凯迪社区猫眼看人 ID sophgold 和 id 丁丁的兰莲花

他们所有的主题,都跟美元黄金有关,全都是围绕这人(谢国忠的小IDhttps://ytilauxes.blogspot.ae/2017/12/20171221708.html)https://ytilauxes.blogspot.de/2017/10/20171061636.html去发帖的

我舅妈自己说,他父亲是崇明人,建国后在上海市区的一家,国营工厂工作

66年前后,工厂要搬迁到西安,我舅妈的父亲就自己一个人去了

他把自己的妻子,儿女,全都留在上海

后来我舅妈发现,自己的母亲,跟别的男人睡在一起,就写信把这件事告诉给她的远在西安的父亲

他父亲大怒,就下令他们全家,他的妻子儿女,全都到西安去生活

在我舅妈适合结婚的年纪

我舅妈的父亲看上了我舅舅,觉得我舅舅聪明,就让我舅舅娶我舅妈

我看到过不少我舅妈我舅舅,以及,我舅妈舅舅生的儿子,三人一起拍的照片

在文革年代,很多人挨批斗,生不如死,我舅舅却拍了一些照片,还有一张照片在北京拍的,拍摄年份是74年,以及后来76年前后认识我舅妈,77年左右结婚,78年生了我表哥

但是别人挨批斗,生不如死的时候,我舅舅没有参与到西安的文革运动中去,也没有斗过任何人

我妈妈家族,就是外公姓傅,外婆姓林,子女等,也算不上是文革逍遥派

因为我阿姨下乡了,得肝炎,我外婆弟弟的老婆干重体力活,热死了,我妈妈上海的亲戚,因为爱漂亮,烫头发,穿小裤脚管长裤,被剪了头发,被剪了裤子,以及上海的亲戚,下乡后跟知青生了孩子,男知青后来被车撞死了,我妈妈亲戚自己带大孩子

还有什么事情,我妈妈还没跟我说过,比如有亲戚在百胜集团工作或者在可口可乐工作,但工作的职位是很艰辛的那种

我妈妈家族,外公外婆,及子女配偶和儿女,就只有这个舅妈,为人处事比较行

但也不是社会上八面玲珑的女强人类型,也不是另一种,擅长散发女人味的那种人

我舅舅也不知是什么原因,事业心不强,跟他一起从事会计职业的同事,都去考职业资格证书,我舅舅却考不过,连会计上岗证都没有

我舅舅舅妈的爱好不太一样

我舅舅喜欢无线电,喜欢摄影,喜欢电器

我舅妈喜欢各种有意思的东西,吃穿用她什么都喜欢

我舅妈喜欢这些,也说明她家庭背景很一般,没什么家底,如果有家底的,家里祖传留下很多好东西,就不会觉得,外面卖什么,她喜欢什么

所以我舅妈舅舅的矛盾就在这里

我舅舅有了钱,就想存起来,他存钱什么意图我也不知道,可能是应对孩子的成长,买各种学习用具,交学费

我舅舅确实给我表哥买了很多很多物品

我表哥有很多很多很多书,他现在很多很多很多书,扔掉了一大半都不止

过去流行连环画,我舅舅给我表哥就买了各种名著的连环画

后来我舅舅又给我表哥买录像带,他们把好看的电视全录下来,我舅舅还喜欢看越剧,也都录下来,录像带录装满了几个抽屉

我舅舅还在流行小霸王学习机时,买给我表哥,以及买各种其他比如游戏机给我表哥

我舅妈具有小资品味,她自己姿色也上乘,所以她最大的遗憾是,没有生一个女儿,这样就可以既打扮自己又打扮女儿

我记得我小时候,我舅妈就打扮我,不过我小时候不好看,很快就长胖了,越打扮越难看

儿时我经常跟我表哥吵架,甚至打架,我跟我表哥在暑假寒假都跟外婆一起渡过

我跟我表哥打架,我舅舅舅妈不会打骂我,但我阿姨会去打骂我表哥,所以我舅妈心疼儿子,就跟我阿姨吵架打架

我跟我表哥打架时,外公外婆在一边劝架,唯独我阿姨会去打骂我表哥。我阿姨现在看到我表哥儿子,像看到杀全家凶手一样,看到我表哥,也像是看到杀父仇人一样

我阿姨跟我表哥从来不联系,我阿姨还仇视我表哥老婆,也跟我表哥老婆和表哥吵过架

我阿姨还跟我舅妈打架,却不是因为小孩的矛盾

我阿姨跟我舅妈两种性格的人

我舅妈看谁都顺眼,跟谁关系都好,喜欢交朋友,喜欢让朋友来家里做客,喜欢到朋友家做客

我阿姨几乎没有朋友,看谁都不顺眼

不过我阿姨姨夫关系很好,他们俩是天生的互补的一队

我也不知道我舅妈为什么跟舅舅离婚

但主要原因还是因为我舅妈出轨

就是很多人说的七年之痒之类的话题

我舅妈出轨以后,我舅妈舅舅离婚了,我舅舅和表哥住在一套1居半室的房子里,我舅妈住在2居室的房子里

后来工厂搬迁,我舅舅表哥住在2居室的房子,我舅妈住在2居室的房子

我舅妈舅舅互相之间也来往,并不是像仇人那样,彼此仇视且老死不相往来

但是我舅妈没有给过我表哥一分钱抚养费,也很少去看我表哥

我表哥很喜欢她妈妈,但是我舅妈不去看望他,我表哥也不会主动去看望自己妈妈

我表哥总是在,我妈妈,我,在西安,跟我舅妈联系的时候,再去看望自己的妈妈

我舅妈跟现在的丈夫一见钟情,闪婚

过到现在也有20多年了

但是我舅妈跟人相处的模式,让我难以理解

就是她在各种人面前,把自己丈夫说得一无是处,但是在家里却跟自己丈夫好得如胶似漆

如果仅仅凭借我舅妈对自己丈夫,不管是哪任的评价,来判断,她自己的婚姻生活是否和睦,其实很难搞清楚她到底过得好不好

我舅妈的性格和脾性,是属于玩性比较大的类型,但是中国自古有句古话,玩物丧志,她的表现虽然不是玩物丧志,但是她确实喜欢玩,她喜欢跟很多人聚在一起,作为聚会之中,众多人之中的焦点,她也喜欢邀请朋友来家里玩

我舅妈另一方面却也是个合格的妻子,她做家务很擅长,尤其擅长做饭,她的收入始终不高,这些收入不足以支撑她过那种,聚会焦点的日子,但她可以,靠自己节约,自己做饭,举办聚会,让自己过得有声有色

她做得一手好菜

我舅妈的丈夫,喜欢的是穿衣打扮,书画摄影,确实有些古语玩物丧志的样子,他还喜欢音乐会乐器弹奏

我舅妈跟自己丈夫在一起,就从过去喜欢穿衣打扮,到现在,省钱让丈夫穿衣打扮

这个丈夫把自己微薄的收入系数交给我舅妈打理,我舅妈再给他一笔零花钱,这个丈夫另外买衣服烟酒,钱是我舅妈出,所以如果任由这个丈夫花钱买烟酒穿衣,家里的钱很快会用完,但是我舅妈却会偷偷存一些钱,而告诉这个丈夫,家中存款其实不多

跟我舅舅在一起,我舅妈却是不存钱

我舅舅一直在工作,工厂破产以后也在工作,所以我舅舅工作之余,积攒了一笔工资收入,我舅舅另外还有奖金收入,直到09年我舅舅突然去世,我舅舅提及他要买房,而当时西安我外婆家小区附近的房价是4000余元一平方米,我舅舅说他不愿意跟外婆住在一起,而是要另外住一套房子,他说他准备买2居室房子,这大概有7,80平米

所以我不知道我舅舅究竟攒了多少钱

我舅妈工作的时候就是插拔电话线,不工作的时候也从来没工作过。

我舅妈的丈夫也没有工作过

但我舅妈的丈夫对外却说自己有个固定工作但其实他一直没工作,但是他不知哪儿来的收入支持他活下去,对外他说他有固定单位一直在单位工作且同事众多,电话本中都是同事的电话号码。

后来为了掩人耳目,我舅妈再婚丈夫和我舅妈,俩人做了一点小生意,就是自己花钱在新疆住了几个月,但钱哪儿来的谁都不知道,卖什么产品也没人知道。在新疆他们俩连天池都去过了,就是在新疆一直游山玩水

他们有很多游山玩水的照片,以前大量的照片贴在QQ相册,现在QQ相册照片全删除了

除去他们在新疆游山玩水几个月住在那里的花费

按照我开始关注他们俩的生活,他们一个月起码跟朋友聚会一次,就是,不是去朋友家,就是朋友来他们家,或是外出在饭店,跟朋友一起聚餐

除此,一个月至少外出旅行一次,旅行指的是离开家,至少在外面住3天以上

一年还要长途旅行至少一次,就是乘火车10几个小时那种

这样模式的生活,从97年98年搬到西安郊区就是如此。他们有大量游山玩水的照片,在数码相机发明以前,这些照片都是胶卷冲印,其中一些游山玩水的照片,跟我妈妈和她们一起聚会的重合,但跟我妈妈聚会的照片,只是很小一部分。后来有了数码相机,就每隔几天传到QQ相册,但最终她自己又删掉了QQ相册的所有照片

我舅妈喜欢成为人群中的焦点,而确实有很多男人围着她转,就连聚会拍照,那些男人都以,可以搂住她拍一张照片而感到喜悦

而我小时候记得,为了跟工厂司机搞好关系,她把工厂司机请到家里,司机脱光上衣,她就在拉上窗帘的阴暗的房间很暧昧的摸司机的背

她交往的司机的妻子叫陈来弟,文革期间的产物,父母希望生个儿子。这个司机五大三粗像混黑社会的,但那时还没有黑社会

我舅舅舅妈关系不好,表面是为了钱,其实是其他方面的问题,主要是我舅妈跟各种男人暧昧不清

但是离异以后他现在的丈夫不管这些事,我舅妈也当现在的丈夫面,提及陈来弟的五大三粗的司机丈夫

我表哥一直跟爷爷奶奶生活,也就是我外公外婆,我表哥的外婆外公全家根本就不喜欢他。后来离异了,我表哥就三餐吃在外公外婆家,没离异以前,三餐吃也吃在外公外婆家

所以我表哥是外公外婆带大的

但是我阿姨说,我表哥是个势利眼,我舅舅死了,外公外婆老了,我表哥就去亲近他妈妈,让他妈妈帮他做这个做那个

我阿姨仇视我表哥,仇视我表哥老婆,仇视我表哥儿子,就像是,他们三个,把阿姨全家上下,杀绝了一样

我表哥也同样仇视我阿姨

我外公外婆老了,最初外公外婆住院,表哥还帮帮忙,后来表哥就再也不管外公外婆了

我阿姨一直工作,最艰辛的工作,工厂倒闭后也是从事最艰辛的工作

但是我阿姨也莫名删除了很多QQ相册的照片,这说明很多年里,至少是5年间,她一直在玩

不知从什么时候起,可能是因为我在网上说了什么言论,引起什么人的警惕,我阿姨,我舅妈等人,包括我表哥,在一夜之间,全都把QQ相册里的,5年多前甚至更早的照片,删除得一张都不剩

我表哥最初在西安的工资不到1000元,这时就已经跟老婆结婚了,她老婆的生活水准,就是在反季节的时候买最贵的水果当饭吃,比如西安的芒果属于反季节水果,她就一天买2,30元芒果,芒果上市几天她吃几天

也不做饭,整天在外面吃饭

到处跟我舅妈一起出去聚会和旅游,不上班,没一分钱收入,买的东西却至少是外资的在国内合资品牌的档次

我妈妈说,她每个月花那么多钱,是我舅舅另外把自己工资和存款贴给她用

但实情是怎么回事,我却不知情

后来她又提出离婚,要求我舅舅支付彩礼,支付赡养费,分我舅舅的房产

我们都觉得这事跟我舅舅没关系

而是我表哥应该出面处理

最终婚没有离,财产没有分,我表哥老婆就病倒了

在病倒以前,他们生了一个孩子,而我舅舅在表哥老婆怀孕时,就死了

我表哥老婆对孩子非常狠毒,经常是恶狠狠毒打自己儿子,并大喊,打死你打死你打死你

但是没多久她就病倒了

我表哥的儿子就被接回了西安

跟自己妈妈我表哥老婆在一起时,我表哥儿子,站着拉屎

我表哥7,8岁的时候,我舅妈就再也不见他了

7,8岁以前,我表哥由外公外婆爸爸带大,我舅妈整天玩,跟各种女友好友在一起玩,还跟其他人在一起玩,比如五大三粗的司机

我表哥没有受到过正常的家庭教育,从小就不懂得自己整理衣物,自己整理书包,用过的东西也不知道自己放回去

所以后来我表哥结婚,跟老婆在一起,俩人喝牛奶,要把塑料袋剪一个三角出来,他们俩就在家里,各个角落,剪了无数个三角,在家的地板或桌上

我表哥老婆大概也是我表哥这样的人,所以表哥老婆有了儿子,就让儿子站着拉屎

我表哥的妈妈我舅妈,离开我表哥以后,跟自己新婚丈夫在一起玩

新婚丈夫有个儿子,但出生时被抱错了,等于这个新婚丈夫生了儿子以后,领到身边的是其他人的孩子

新婚丈夫没有养育过自己的,并不知情的“亲生”儿子

这个“亲生”儿子,由自己妻子抚养

新婚丈夫后来跟妻子离婚了,90年代就跟我舅妈结婚

所以我舅妈,和新婚丈夫,都不是爱孩子的成年人

他们俩的婚姻,在双方都没有孩子的负担下,过得很好,整天就是玩

我表哥有了孩子以后,没有麻烦自己亲妈,让她带孩子

而是我表哥自己跟老婆,201几年时,全都去了深圳,把孩子也带去了深圳

但后来他们出意外,表哥老婆病倒了,病倒以前表哥老婆对孩子也不好

最终就只有我表哥的妈妈,表哥妈妈新婚丈夫,俩人一起,带我表哥的孩子

我表哥的儿子,成长过程中

父亲,母亲,两个双亲的角色,缺位

所以表哥儿子的性格,为人处事,都有点问题

而我表哥的妈妈的新婚丈夫,可能非常嫉恨我表哥的妈妈

在我表哥儿子成长的每个点滴,哪怕学说话,以及学习跟长辈相处的过程中

都不断向我表哥儿子灌输各种奇怪的观点

我表哥儿子就变得越来越霸道,而且对奶奶,也就是我表哥的妈妈的态度,越来越不好

我亲眼见过这种情形

我认为小孩就是记性差,不记仇,但是大人在孩子面前灌输什么观点,日子久了,小孩就会形成什么观点,并对某些事情,做出条件反射般的回应

http://www.tianya.cn/27077215/bbs 这人发贴提到那么多事情,

比如天涯网站有个ID sophgold 还有个ID 克莱因瓶里的猫

以及凯迪社区猫眼看人 ID sophgold 和 id 丁丁的兰莲花

他们所有的主题,都跟美元黄金有关,全都是围绕这人(谢国忠的小IDhttps://ytilauxes.blogspot.ae/2017/12/20171221708.html)https://ytilauxes.blogspot.de/2017/10/20171061636.html去发帖的

2016年8月29日星期一

85年86年一场电影,不整容女星,下生活体验角色演员和导演,电影票售价0.3元到0.5元

现在整容女星,不体验生活,剧中出现外语台词,用配音

一场电影,团购30元一张票

85,86年,普遍的收入是50元到70元,收入是电影票的140倍

现在最低收入不到2000,收入是电影票的60余倍

一场电影,团购30元一张票

85,86年,普遍的收入是50元到70元,收入是电影票的140倍

现在最低收入不到2000,收入是电影票的60余倍

2016年8月23日星期二

601988中国银行年报,分析,续

2015年3月我跟我妈妈去香港,在香港的酒店,我不用翻墙就看了几个,在中国境内却需要翻墙才能看到的软件

其中FT中文网,罗斯柴尔德家族成员,又跳出来,或者说,是FT中文网的编辑人员,又把过去刊登过的,罗斯柴尔德家族成员的一篇采访稿,又刊登出来

我从来不看FT中文网,也不看动态网,更是不看华尔街日报(动态网是金盾工程建立以来,建立的网站。直到2006年,动态网的网址链接,其中的网站比如华尔街日报网等,都无须翻墙浏览)

比如我一直认为动态网新唐人大纪元电视节目中有几个人,在电视节目中的说话口吻,就是个流氓腔

FT中文网,动态网,德国之声,BBC中文网,美国之音,华尔街日报

这些都是动态网这个网站的链接,其中是以薄熙来江泽民胡锦涛曾庆红等人建立的

这些人都跟微软的比尔盖茨在中国做生意

我喜欢用一个人的文笔来判断我是不是应该看对方的文字

比如年纪大的,5,60岁以上的人

我以文革66年以前他她读过中学就是初三毕业为基准,读过的,符合条件一

又以78年文革结束,他她继续读高中大学以及大学本科毕业再出国读书,为条件二

符合这样条件的人,文笔一般不会很差,就是我愿意读的那些人的文章

同龄人就是79年80年的,我以211院校毕业为标准

然而FT中文网,各种人的聚集地,都是文革时的红卫兵,以及文革后没读过书,直接就去做生意的

这部电影Mementohttp://ytilauxes.blogspot.com/2016/08/something-in-air.html是个刑事案,主角没有长期记忆,比如他拿一张纸,看到纸上写着一段话,他读过以后,过一会儿就会忘记了

以及,他见到一个人,记住他的名字,记住他的长相,过一会儿也忘记了

但是我还没有到这个地步

薄熙来的圈子,包括胡耀邦,但我不知道赵紫阳是哪个圈子的,赵紫阳的父亲是个小地主,文革赵紫阳也有过革命的行为,斗过他的地主父亲

薄熙来现在让一个工人的女儿姜丰,代表地主的后代,在公众面前发言,然而真正的地主后人,建立的网站,却莫名从互联网上消失了

薄熙来和王震家人,现在力挺的是毛泽东,共济会也挺毛泽东,中国的纸币,就只有毛泽东一个人的头像

毛泽东的什么行为,我全都不知道,但是我妈妈他们知道,比如王震家人建立的微信群,我妈妈的西安同事朋友,这些都是毛泽东时代的产物

现在习近平也有毛泽东倾向

跟美国金融界或世界金融界互相之间股权错综复杂的一个叫草根网www.caogen.com/的网站,我的从小到大的生活,以及该见什么人,去哪儿,甚至每次外出,都是这个网站草根网 www.caogen.com 的人安排的和一个叫gewenwei的人安排的 https://www.zhihu.com/people/gewenwei。我的言论对准了控制中国大量资产的政府,以及草根网 www.caogen.com 的人,从2016年7月起安排我生活的人,就开始,在我每天所遇到的各种事,各种人之中,刻意设置各种障碍,来刁难我,为难我。整个上海市也跟这个 www.caogen.com 草根网和gewenwei https://www.zhihu.com/people/gewenwei有关,我只要一走出家门,就整天不管走到哪儿,在家门口附近,在家附近1公里范围,在市区,在任何地方,都有人给我设置各种障碍,刁难为,为难我,让我不能很顺利得做成一件事,什么叫顺利,就是比如去便利店缴费,顺利的意思就是,别人收钱办事,没有节外生枝。而我总是遇到各种节外生枝,去便利缴费,买东西,哪怕走在路上,也会突然冒出一个,就是这个网站 http://www.caogen.com 草根网,gewenwei https://www.zhihu.com/people/gewenwei以及政府部门的特工人员,故意装扮成各种样子的人,哪怕恶狠狠瞪我一眼,他们也会觉得他们做到了刁难为,为难我

比如我发现其中一个也参与过文革的女人,她写的文章,说起她在文革期间暴力行为,她说文革她在上海市吴淞口军训

这个女人的文章,也发表在温家宝等人一起发表文章的,炎黄春秋杂志。这女人姓王,就生活在上海或者宝山区的吴淞,她说自己小学学历,下岗了,我看了她博客,她整天谈论的都是国家大事。后来炎黄春秋杂志把这个文革有过暴力行为的王姓下岗女工的文章,全隐藏起来了

在中国控制货币供应控制物价的,也是这个叫草根网http://www.caogen.com/上面的人,只要我的言论不符这些文革余虐http://www.caogen.com/的心意,而他们也不给我钱,我就会面临,吃不起饭的局面

余虐们写文章给人洗脑,说货币事关伦理,伦理就是无缘无故打死人吗或者干各种伤害他人的事?

文革余虐,把一个跟我在网上零交流的人,让他在网上说我整天关心政治

而这是文革余虐的爱好,不是我的爱好

我对政治的关注是零,我是个政治盲,要不是有人写各种政治文章,我连选举是每个国家都在做的事我也不知道,我唯一上过的政治课就是从小学到大学的政治课

文革余虐莫名把06年关注政治的韩寒跟我搅和在一起,然而我在06年的真实意图是,我更喜欢关注文化

而我关注的文化,也不是网上主动搭理我,他们关注的黑暗文化http://ytilauxes.blogspot.ae/2016/07/all-dark-arts-have-their-own-will.html

我在网上零星关注的政治,就是文革余虐的做恶,各种暴力行为。但是现在各行各业,掌权的都是文革余虐,而我一开始上网就不喜欢毛泽东,文革余虐又说我是林昭投胎转世。还说我自己做林昭搞得自己艰难却连累家人也艰难http://ytilauxes.blogspot.com/2016/07/721.html

其中FT中文网,罗斯柴尔德家族成员,又跳出来,或者说,是FT中文网的编辑人员,又把过去刊登过的,罗斯柴尔德家族成员的一篇采访稿,又刊登出来

我从来不看FT中文网,也不看动态网,更是不看华尔街日报(动态网是金盾工程建立以来,建立的网站。直到2006年,动态网的网址链接,其中的网站比如华尔街日报网等,都无须翻墙浏览)

比如我一直认为动态网新唐人大纪元电视节目中有几个人,在电视节目中的说话口吻,就是个流氓腔

FT中文网,动态网,德国之声,BBC中文网,美国之音,华尔街日报

这些都是动态网这个网站的链接,其中是以薄熙来江泽民胡锦涛曾庆红等人建立的

这些人都跟微软的比尔盖茨在中国做生意

我喜欢用一个人的文笔来判断我是不是应该看对方的文字

比如年纪大的,5,60岁以上的人

我以文革66年以前他她读过中学就是初三毕业为基准,读过的,符合条件一

又以78年文革结束,他她继续读高中大学以及大学本科毕业再出国读书,为条件二

符合这样条件的人,文笔一般不会很差,就是我愿意读的那些人的文章

同龄人就是79年80年的,我以211院校毕业为标准

然而FT中文网,各种人的聚集地,都是文革时的红卫兵,以及文革后没读过书,直接就去做生意的

这部电影Mementohttp://ytilauxes.blogspot.com/2016/08/something-in-air.html是个刑事案,主角没有长期记忆,比如他拿一张纸,看到纸上写着一段话,他读过以后,过一会儿就会忘记了

以及,他见到一个人,记住他的名字,记住他的长相,过一会儿也忘记了

但是我还没有到这个地步

薄熙来的圈子,包括胡耀邦,但我不知道赵紫阳是哪个圈子的,赵紫阳的父亲是个小地主,文革赵紫阳也有过革命的行为,斗过他的地主父亲

薄熙来现在让一个工人的女儿姜丰,代表地主的后代,在公众面前发言,然而真正的地主后人,建立的网站,却莫名从互联网上消失了

薄熙来和王震家人,现在力挺的是毛泽东,共济会也挺毛泽东,中国的纸币,就只有毛泽东一个人的头像

毛泽东的什么行为,我全都不知道,但是我妈妈他们知道,比如王震家人建立的微信群,我妈妈的西安同事朋友,这些都是毛泽东时代的产物

现在习近平也有毛泽东倾向

跟美国金融界或世界金融界互相之间股权错综复杂的一个叫草根网www.caogen.com/的网站,我的从小到大的生活,以及该见什么人,去哪儿,甚至每次外出,都是这个网站草根网 www.caogen.com 的人安排的和一个叫gewenwei的人安排的 https://www.zhihu.com/people/gewenwei。我的言论对准了控制中国大量资产的政府,以及草根网 www.caogen.com 的人,从2016年7月起安排我生活的人,就开始,在我每天所遇到的各种事,各种人之中,刻意设置各种障碍,来刁难我,为难我。整个上海市也跟这个 www.caogen.com 草根网和gewenwei https://www.zhihu.com/people/gewenwei有关,我只要一走出家门,就整天不管走到哪儿,在家门口附近,在家附近1公里范围,在市区,在任何地方,都有人给我设置各种障碍,刁难为,为难我,让我不能很顺利得做成一件事,什么叫顺利,就是比如去便利店缴费,顺利的意思就是,别人收钱办事,没有节外生枝。而我总是遇到各种节外生枝,去便利缴费,买东西,哪怕走在路上,也会突然冒出一个,就是这个网站 http://www.caogen.com 草根网,gewenwei https://www.zhihu.com/people/gewenwei以及政府部门的特工人员,故意装扮成各种样子的人,哪怕恶狠狠瞪我一眼,他们也会觉得他们做到了刁难为,为难我

比如我发现其中一个也参与过文革的女人,她写的文章,说起她在文革期间暴力行为,她说文革她在上海市吴淞口军训

这个女人的文章,也发表在温家宝等人一起发表文章的,炎黄春秋杂志。这女人姓王,就生活在上海或者宝山区的吴淞,她说自己小学学历,下岗了,我看了她博客,她整天谈论的都是国家大事。后来炎黄春秋杂志把这个文革有过暴力行为的王姓下岗女工的文章,全隐藏起来了

在中国控制货币供应控制物价的,也是这个叫草根网http://www.caogen.com/上面的人,只要我的言论不符这些文革余虐http://www.caogen.com/的心意,而他们也不给我钱,我就会面临,吃不起饭的局面

余虐们写文章给人洗脑,说货币事关伦理,伦理就是无缘无故打死人吗或者干各种伤害他人的事?

文革余虐,把一个跟我在网上零交流的人,让他在网上说我整天关心政治

而这是文革余虐的爱好,不是我的爱好

我对政治的关注是零,我是个政治盲,要不是有人写各种政治文章,我连选举是每个国家都在做的事我也不知道,我唯一上过的政治课就是从小学到大学的政治课

文革余虐莫名把06年关注政治的韩寒跟我搅和在一起,然而我在06年的真实意图是,我更喜欢关注文化

而我关注的文化,也不是网上主动搭理我,他们关注的黑暗文化http://ytilauxes.blogspot.ae/2016/07/all-dark-arts-have-their-own-will.html

我在网上零星关注的政治,就是文革余虐的做恶,各种暴力行为。但是现在各行各业,掌权的都是文革余虐,而我一开始上网就不喜欢毛泽东,文革余虐又说我是林昭投胎转世。还说我自己做林昭搞得自己艰难却连累家人也艰难http://ytilauxes.blogspot.com/2016/07/721.html

2016年8月22日星期一

就是从2016年7月15日16日起,我更新了几则博客,就哪个翻墙软件都不能用,也不能上传照片了

http://ytilauxes.blogspot.ae/2016/07/weathercomcn.html

http://ytilauxes.blogspot.ae/2016/07/blog-post_14.html

http://ytilauxes.blogspot.ae/2016/07/blog-post_52.html

http://ytilauxes.blogspot.ae/2016/07/blog-post_22.html

http://ytilauxes.blogspot.ae/2016/07/blog-post_94.html

http://ytilauxes.blogspot.ae/2016/07/0656.html

http://ytilauxes.blogspot.ae/2016/07/06pfizerpfizer.html

http://ytilauxes.blogspot.ae/2016/07/601611ipo.html

http://ytilauxes.blogspot.ae/2016/07/blog-post_40.html

http://ytilauxes.blogspot.ae/2016/07/20.html

http://ytilauxes.blogspot.ae/2016/07/blog-post_14.html

http://ytilauxes.blogspot.ae/2016/07/blog-post_52.html

http://ytilauxes.blogspot.ae/2016/07/blog-post_22.html

http://ytilauxes.blogspot.ae/2016/07/blog-post_94.html

http://ytilauxes.blogspot.ae/2016/07/0656.html

http://ytilauxes.blogspot.ae/2016/07/06pfizerpfizer.html

http://ytilauxes.blogspot.ae/2016/07/601611ipo.html

http://ytilauxes.blogspot.ae/2016/07/blog-post_40.html

http://ytilauxes.blogspot.ae/2016/07/20.html

2016年8月21日星期日

35,110,55,18,90,23,42,50

我算了一下帐

我们每月水费35元,平摊到每天是一元

宽带每月110元,平摊到每天是4元左右

电信手机,通话时间,不区分国内跨省市还是本市,600分钟通话时间,以及240M全国通用上网流量,还可以带4张副卡,副卡号码跟主卡不同,但,副卡的通话时间和上网流量,都在主卡的使用范围内,55月一个月费用,平均每天不到2元

移动的手机几乎不对外拨打电话,有不到100M流量,18元一个月,平均0.6元一天

电费90元一个月,平均每天3元

有线电视费23元一个月,平均每天1元

物业费42元一个月,平均每天不到1.5元

煤气费50元一个月,平均每天不到1.7元

加总起来

水费,宽带费,电信手机,移动手机,电费,有线电视费,物业费,煤气费

2015年2016年,平均一个月,近500元。而2002年11,12月份起我自己租房,我交水,电,手机,物业,宽带,不交煤气,有线电视,少交一个手机,一个月费用,不到150元

用电,比如今年8月是天天高温没下过雨,也不会超过150元,一个月,以及去年冬天,每天都零下4到5度,也不会超过200元一个月

水就是天天洗澡,天天洗菜,洗衣服,冲马桶

煤气就是自己做饭,以及用燃气热水器

我们每月水费35元,平摊到每天是一元

宽带每月110元,平摊到每天是4元左右

电信手机,通话时间,不区分国内跨省市还是本市,600分钟通话时间,以及240M全国通用上网流量,还可以带4张副卡,副卡号码跟主卡不同,但,副卡的通话时间和上网流量,都在主卡的使用范围内,55月一个月费用,平均每天不到2元

移动的手机几乎不对外拨打电话,有不到100M流量,18元一个月,平均0.6元一天

电费90元一个月,平均每天3元

有线电视费23元一个月,平均每天1元

物业费42元一个月,平均每天不到1.5元

煤气费50元一个月,平均每天不到1.7元

加总起来

水费,宽带费,电信手机,移动手机,电费,有线电视费,物业费,煤气费

2015年2016年,平均一个月,近500元。而2002年11,12月份起我自己租房,我交水,电,手机,物业,宽带,不交煤气,有线电视,少交一个手机,一个月费用,不到150元

用电,比如今年8月是天天高温没下过雨,也不会超过150元,一个月,以及去年冬天,每天都零下4到5度,也不会超过200元一个月

水就是天天洗澡,天天洗菜,洗衣服,冲马桶

煤气就是自己做饭,以及用燃气热水器

diligent and thrifty勤俭节约

送的各种团购的代金券,美团,大众点评,糯米,全都用不了

就是点击代金券,使用,却

无法使用

后来糯米送的代金券,再点击进去,一看,修改成为,已经过期了

不过大众点评网,送的一个代金券,8元的,却可以用

我还遇到一件怪事,就是我注册了肯德基的会员,买了39元券5顿早餐,我全吃掉了,还另外付钱买了一只早餐的汉堡

两天吃掉5顿早餐,1只汉堡,第一天吃2顿早餐,1个汉堡,第二天吃三顿早餐

第一天的积分,审核了很久却不给我,最终也给我了

第二天的三顿早餐的积分,却不给我了

送的团购优惠券,比如没有优惠条件的前提下,买一份午餐要花费23元,但有优惠券就花费16元,结果用了优惠券,便宜了7元,再加一份餐,最终,拿到手的却是,一份午餐的量。店家把便宜给用户的7元,从少给一份午餐中,赚了回来

所以我就不再用那些优惠价格很大的团购券了

就是点击代金券,使用,却

无法使用

后来糯米送的代金券,再点击进去,一看,修改成为,已经过期了

不过大众点评网,送的一个代金券,8元的,却可以用

我还遇到一件怪事,就是我注册了肯德基的会员,买了39元券5顿早餐,我全吃掉了,还另外付钱买了一只早餐的汉堡

两天吃掉5顿早餐,1只汉堡,第一天吃2顿早餐,1个汉堡,第二天吃三顿早餐

第一天的积分,审核了很久却不给我,最终也给我了

第二天的三顿早餐的积分,却不给我了

送的团购优惠券,比如没有优惠条件的前提下,买一份午餐要花费23元,但有优惠券就花费16元,结果用了优惠券,便宜了7元,再加一份餐,最终,拿到手的却是,一份午餐的量。店家把便宜给用户的7元,从少给一份午餐中,赚了回来

所以我就不再用那些优惠价格很大的团购券了

2016年8月20日星期六

Internet of Things,缩写IoT,物联网

我们搬家以后,买的家电,看起来都是杂牌,但却是,暗中

具备

物联网功能的家电

物联网我理解的本意

就是可以远程操控家中的电器

比如

远程,在下班前,让家中空调打开,或让家中电热水器开始工作,以及远程,让电饭煲做饭等

然而物联网功能

却可以让黑客

去控制,不是自己家,而是别人家的

家用电器的开关

我自己的家电,就遇到,被人使用物联网功能的设备,远程,改了设置,以及远程关闭或启动我家里的家电的现象

具备

物联网功能的家电

物联网我理解的本意

就是可以远程操控家中的电器

比如

远程,在下班前,让家中空调打开,或让家中电热水器开始工作,以及远程,让电饭煲做饭等

然而物联网功能

却可以让黑客

去控制,不是自己家,而是别人家的

家用电器的开关

我自己的家电,就遇到,被人使用物联网功能的设备,远程,改了设置,以及远程关闭或启动我家里的家电的现象

ftp功能

我刚上网的时候

下载免费的音频格式的mp3文件,下载免费的电影等

都是从ftp网站上下载的

我也不知道ftp的原理是什么

大致的意思是,文件在他人的硬盘空间里,然后通过互联网,读取他人硬盘里的资料

德国人发明的napster下载软件,也是从他人硬盘空间里,读取文件,互相分享,或者供人下载

今天我用到了

把ftp功能,用于

手机内的文件,跟自己台式机,互相之间连接http://ytilauxes.blogspot.com/2016/08/wireless-fidelity-bluetooth.html

然后台式机就可以直接读取,手机里的文件

手机的文件,传输到台式机

不需要用到数据线

这个功能

使我想起

全球监视每个活生生的个人的事例

就是每个人,只要使用电子设备,这个电子设备,哪怕

表面上

没有连接互联网

但它实际还是会具备ftp的功能

就是他人,比如说监视你的人,可以

远程,读取你电子设备里的每一个信息

类似的事例,我提及过很多次

比如,我把手机sim卡拿掉了,但是外面打来的电话

手机继续响铃,并显来电l号码http://ytilauxes.blogspot.com/2016/04/sim.html

以及,没有sim卡的前提下,手机可以对外拨打号码,比如拨打110

理论上,没有sim卡,甚至可以拨打任何号码

ps.我还把sim卡剪掉了,想看看里面是些什么,但实际就是一层假装像金属涂层的物质,下面是一块硬的东西,像是碳这种材料做的,这张卡纯粹是个摆设

我的手机在使用过程中

我发现,我自己存在手机里的,他人的名字,电话号码,全都存在移动或电信的计算机机房里(一个叫《互联网》的纪录片http://www.iqiyi.com/a_19rrhc0sx9.html,也有这样的情节在里面,而我看这个纪录片5-10集时,天气一下子变得很不好,黑云压城,纪录片的内容就是,技术带来负面效应,比如黑客可以起破坏作用)

在我的sim卡失效时,或者sim卡储存的信息全都没有了的时候,这些被存储在移动或电信的计算机房里的信息,却还都在

比如说,我可以要求移动或电信,把我过往使用手机,保存的他人信息和电话号码,全都转发给我,如果我有这样的权限的话

发送过的短信也是如此

下载免费的音频格式的mp3文件,下载免费的电影等

都是从ftp网站上下载的

我也不知道ftp的原理是什么

大致的意思是,文件在他人的硬盘空间里,然后通过互联网,读取他人硬盘里的资料

德国人发明的napster下载软件,也是从他人硬盘空间里,读取文件,互相分享,或者供人下载

今天我用到了

把ftp功能,用于

手机内的文件,跟自己台式机,互相之间连接http://ytilauxes.blogspot.com/2016/08/wireless-fidelity-bluetooth.html

然后台式机就可以直接读取,手机里的文件

手机的文件,传输到台式机

不需要用到数据线

这个功能

使我想起

全球监视每个活生生的个人的事例

就是每个人,只要使用电子设备,这个电子设备,哪怕

表面上

没有连接互联网

但它实际还是会具备ftp的功能

就是他人,比如说监视你的人,可以

远程,读取你电子设备里的每一个信息

类似的事例,我提及过很多次

比如,我把手机sim卡拿掉了,但是外面打来的电话

手机继续响铃,并显来电l号码http://ytilauxes.blogspot.com/2016/04/sim.html

以及,没有sim卡的前提下,手机可以对外拨打号码,比如拨打110

理论上,没有sim卡,甚至可以拨打任何号码

ps.我还把sim卡剪掉了,想看看里面是些什么,但实际就是一层假装像金属涂层的物质,下面是一块硬的东西,像是碳这种材料做的,这张卡纯粹是个摆设

我的手机在使用过程中

我发现,我自己存在手机里的,他人的名字,电话号码,全都存在移动或电信的计算机机房里(一个叫《互联网》的纪录片http://www.iqiyi.com/a_19rrhc0sx9.html,也有这样的情节在里面,而我看这个纪录片5-10集时,天气一下子变得很不好,黑云压城,纪录片的内容就是,技术带来负面效应,比如黑客可以起破坏作用)

在我的sim卡失效时,或者sim卡储存的信息全都没有了的时候,这些被存储在移动或电信的计算机房里的信息,却还都在

比如说,我可以要求移动或电信,把我过往使用手机,保存的他人信息和电话号码,全都转发给我,如果我有这样的权限的话

发送过的短信也是如此

2016年8月18日星期四

Revolution to Riches

http://topics.bloomberg.com/revolution-to-riches/

我在博客上提及,跟这个报道有关的人或事http://topics.bloomberg.com/revolution-to-riches/

却发现,自2016年2月初以来,总之我收到的水费单子写着开票日期是2016年2月18日

以往的水费都是一个月平均用18立方

而2016年2月18日以来,水费的用水量,突然,被

城投控股集团,股票代码600649(就是这些人控制的大量资产决定中国经济http://www.51paper.net/ueditor/php/upload/file/20151117/1447740718123298.pdf,www.caogen.com/ 城投控股只是其中之一http://topics.bloomberg.com/revolution-to-riches/)

寄来的账单,3和4月本该18立方的用水量,却增加到了41立方

实际用水没那么多

却莫名增加了20多立方的用水量

而到了2016年6月份,计算的是5和6月份用水总量,更是

莫名增加了40几立方的用水量

2016年8月份,计算的是7和8月份用水总量

莫名增加了60几立方用水量

可是以往一年多来的账单,即便夏季用水高峰月份,用电的费用跟今年夏天一样,说明气温也一样,而用水量也恒定在18立方

此外,citic王震家族,勾结的政府部门和军方,整整近3个月,就是不给上海人工降雨,而最近几天,上海的云层条件,有人工降雨的可能和机会,人工降雨就可以渡过高温,但是citic中信王震家族,宁愿让人污染环境,用煤电等,也不愿让人享受自然凉风http://shenlei929.blogspot.de/2016/05/blog-post.html

我妈保存了一年多的水电煤等费用的单子,去年7月电费是不到100元,8月下旬我们去了西安,10月份才回上海。今年7月电费是120元,8月电费也不会超过150元。今年7月120多元的电费,用了180多度电。http://ytilauxes.blogspot.com/2016/08/blog-post.html http://ytilauxes.blogspot.com/2016/07/polystyrene.html

我在博客上提及,跟这个报道有关的人或事http://topics.bloomberg.com/revolution-to-riches/

却发现,自2016年2月初以来,总之我收到的水费单子写着开票日期是2016年2月18日

以往的水费都是一个月平均用18立方

而2016年2月18日以来,水费的用水量,突然,被

城投控股集团,股票代码600649(就是这些人控制的大量资产决定中国经济http://www.51paper.net/ueditor/php/upload/file/20151117/1447740718123298.pdf,www.caogen.com/ 城投控股只是其中之一http://topics.bloomberg.com/revolution-to-riches/)

寄来的账单,3和4月本该18立方的用水量,却增加到了41立方

实际用水没那么多

却莫名增加了20多立方的用水量

而到了2016年6月份,计算的是5和6月份用水总量,更是

莫名增加了40几立方的用水量

2016年8月份,计算的是7和8月份用水总量

莫名增加了60几立方用水量

可是以往一年多来的账单,即便夏季用水高峰月份,用电的费用跟今年夏天一样,说明气温也一样,而用水量也恒定在18立方

此外,citic王震家族,勾结的政府部门和军方,整整近3个月,就是不给上海人工降雨,而最近几天,上海的云层条件,有人工降雨的可能和机会,人工降雨就可以渡过高温,但是citic中信王震家族,宁愿让人污染环境,用煤电等,也不愿让人享受自然凉风http://shenlei929.blogspot.de/2016/05/blog-post.html

我妈保存了一年多的水电煤等费用的单子,去年7月电费是不到100元,8月下旬我们去了西安,10月份才回上海。今年7月电费是120元,8月电费也不会超过150元。今年7月120多元的电费,用了180多度电。http://ytilauxes.blogspot.com/2016/08/blog-post.html http://ytilauxes.blogspot.com/2016/07/polystyrene.html

2016年8月16日星期二

Freegate自由门软件,不仅是王震家族后人,同时也是江泽民家后人,又是胡锦涛薄熙来家后人,弄的一个翻墙软件。2016年8月起也开始难以使用了

psiphon赛风,翻墙软件,翻出去,点击谷歌首页,IP地址是

127.0.0.1

点击谷歌的域名,不是.com,却是 de

说明,连接英国VPN,只是表象,实际是连接德国的VPN线路,在翻墙

我用的赛风,连接的线路是德国

我发现不管是用freegate还是psiphon,都会出现,长时间无法上传图片文件的现象

后来我意识到,是翻墙软件,故意用这个小缺点,在偷取我硬盘里的文件

德国人偷取我硬盘里的文件,不知什么意思(但这也可能是伪装的假象)

另外,我看一个叫周奇奇的演员,她在新浪微博的账号zhouqiqi627,以数字,6和7结尾http://ytilauxes.blogspot.ae/2016/08/dear-translator.html

共济会的网站,天涯论坛,我曾经回一个,提及朱镕基,这个名字的诸多帖子的一个人的发帖http://www.tianya.cn/27077215/bbs

我在网上回了一些贴,其中

我自己主动

提了数字6和数字7

后来我还回帖,把一些提及

朱镕基,这个人名字的一些贴,回到了我自己跟帖下面

周奇奇曾经代言chinaren这个网站

我想起自己曾经在chinaren找过我一个高中同学,但我没找到这人

现在我想起他的名字叫 yu于余俞 jun 俊骏峻 hui辉晖 我也不知道他名字到底怎么拼写的,他是5班的一个男生

06年的时候,我以为韩寒在新浪回应我的文字,以及韩寒和徐静蕾共同好友圈,都说我应该跟韩寒见面之类的话

但是后来徐静蕾似乎在回应我,说我本来要做女强人,最终却选择做女神之类的话,徐静蕾还说我是当代阮玲玉

我没有搭理徐静蕾也没有搭理韩寒

但我确实不喜欢跟文化人打交道。我看的文化作品,男女,不管唱歌,演戏,都是长得很好看类型的

我后来还因为看了徐静蕾八卦,而自己去批发市场买很多东西,我说我要自己开店,当时我还对胡锦涛提出的八荣八耻这个口号很有好感

但我也干不了体力劳动活

06年时,韩寒后来还弄了几个MV

我在看到他制作的MV之前,我就已经去小店里买各种东西,我说我要开店卖东西

然而06年有人给我吃药,我自己审美其实很好,所以06年我买的物品都不那么好看

后来我记得,就是最近几年,我回过头去看张五常的文章

张五常提及,有人不懂审美的话题,不知是不是在说06年的我

张五常真实的身份是被美国驱逐出境类似的身份,他在美国是个刑事罪犯一旦进入美国境内就必须去坐牢,然而在中国他却是小偷,农民,和尚,回族穆斯林后裔出身的朱元璋后代朱镕基的御用经济学家

另外谢国忠好像写文章提及竞争和道德的话题

06年我也因为我一直在对他人做道德判断,而搞得自己嚎啕大哭

我用的赛风,连接的线路是德国

我发现不管是用freegate还是psiphon,都会出现,长时间无法上传图片文件的现象

后来我意识到,是翻墙软件,故意用这个小缺点,在偷取我硬盘里的文件

德国人偷取我硬盘里的文件,不知什么意思(但这也可能是伪装的假象)

另外,我看一个叫周奇奇的演员,她在新浪微博的账号zhouqiqi627,以数字,6和7结尾http://ytilauxes.blogspot.ae/2016/08/dear-translator.html

共济会的网站,天涯论坛,我曾经回一个,提及朱镕基,这个名字的诸多帖子的一个人的发帖http://www.tianya.cn/27077215/bbs

我在网上回了一些贴,其中

我自己主动

提了数字6和数字7

后来我还回帖,把一些提及

朱镕基,这个人名字的一些贴,回到了我自己跟帖下面

周奇奇曾经代言chinaren这个网站

我想起自己曾经在chinaren找过我一个高中同学,但我没找到这人

现在我想起他的名字叫 yu于余俞 jun 俊骏峻 hui辉晖 我也不知道他名字到底怎么拼写的,他是5班的一个男生

06年的时候,我以为韩寒在新浪回应我的文字,以及韩寒和徐静蕾共同好友圈,都说我应该跟韩寒见面之类的话

但是后来徐静蕾似乎在回应我,说我本来要做女强人,最终却选择做女神之类的话,徐静蕾还说我是当代阮玲玉

我没有搭理徐静蕾也没有搭理韩寒

但我确实不喜欢跟文化人打交道。我看的文化作品,男女,不管唱歌,演戏,都是长得很好看类型的

我后来还因为看了徐静蕾八卦,而自己去批发市场买很多东西,我说我要自己开店,当时我还对胡锦涛提出的八荣八耻这个口号很有好感

但我也干不了体力劳动活

06年时,韩寒后来还弄了几个MV

我在看到他制作的MV之前,我就已经去小店里买各种东西,我说我要开店卖东西

然而06年有人给我吃药,我自己审美其实很好,所以06年我买的物品都不那么好看

后来我记得,就是最近几年,我回过头去看张五常的文章

张五常提及,有人不懂审美的话题,不知是不是在说06年的我

张五常真实的身份是被美国驱逐出境类似的身份,他在美国是个刑事罪犯一旦进入美国境内就必须去坐牢,然而在中国他却是小偷,农民,和尚,回族穆斯林后裔出身的朱元璋后代朱镕基的御用经济学家

另外谢国忠好像写文章提及竞争和道德的话题

06年我也因为我一直在对他人做道德判断,而搞得自己嚎啕大哭

目前中国空置的房子足够30多亿人口在城镇居住,而有线电视披露的数据,中国装有线电视的用户达到20多亿,也就是说中国实际人口超过40亿人

我去过的北京上海无锡杭州成都我妈妈去过广州我家人在深圳,30岁以上就没有人招工了

如题 http://ytilauxes.blogspot.com/2016/07/708777815.html

70年代初中国总人口数8亿多,而计划生育政策是77年78年开始执行的,我估计中国现在的总人口数超过15亿

8亿多总人口数,按照当时的家庭结构来看,育龄男女占2亿人口,18岁以前成年儿童占3亿人口,过了生育年龄的50岁以上男女占3亿人口

这2亿人口育龄男女,有一部分在70年到78年期间,有些夫妻生育了2到3个孩子,比如我就接触过不少这样的家庭,这样家庭中的18岁以下的儿童,年纪都比我大,我是79年生的。这9年间,人口增加了至少1.5亿。总人口就是9.5亿

78年以后,以知识分子和工人家庭为主的育龄男女,大多数都生育了1个孩子。工人的人数难以统计,知识分子人数也难以统计,比如曾经有数据披露,工人有3000多万,还有最近数据披露,事业单位就业人数4000多万。

78年到2018年,整整40年。不知又生育了多少人口。

如题 http://ytilauxes.blogspot.com/2016/07/708777815.html

70年代初中国总人口数8亿多,而计划生育政策是77年78年开始执行的,我估计中国现在的总人口数超过15亿

8亿多总人口数,按照当时的家庭结构来看,育龄男女占2亿人口,18岁以前成年儿童占3亿人口,过了生育年龄的50岁以上男女占3亿人口

这2亿人口育龄男女,有一部分在70年到78年期间,有些夫妻生育了2到3个孩子,比如我就接触过不少这样的家庭,这样家庭中的18岁以下的儿童,年纪都比我大,我是79年生的。这9年间,人口增加了至少1.5亿。总人口就是9.5亿

78年以后,以知识分子和工人家庭为主的育龄男女,大多数都生育了1个孩子。工人的人数难以统计,知识分子人数也难以统计,比如曾经有数据披露,工人有3000多万,还有最近数据披露,事业单位就业人数4000多万。

78年到2018年,整整40年。不知又生育了多少人口。

0700 (HKG)腾讯网

我妈妈把手机留在家里,我看了一些,王姓作为股东, 0700 (HKG)腾讯网,技术人员,以我妈妈家人朋友名义,转发的文章

我回想自己上网历程

我对于娱乐圈,各种明星绯闻,都不怎么关注

我没有窥私癖

然而王姓作为股东的各种权贵太子党成员

却有

拆散他人婚姻

不仅包括娱乐明星

也包括其他不是他们权贵成员的

社会

各阶层人士的各种夫妻的婚姻组合的爱好

我回想自己上网历程

我对于娱乐圈,各种明星绯闻,都不怎么关注

我没有窥私癖

然而王姓作为股东的各种权贵太子党成员

却有

拆散他人婚姻

不仅包括娱乐明星

也包括其他不是他们权贵成员的

社会

各阶层人士的各种夫妻的婚姻组合的爱好

Fed QE China’s yuan devaluation Fed Raise Rates

简单的打个比方

1美元可以兑换2元人民币

美国人或其他国家的人,把货币兑换成美元,拿到中国来,1万美元就有2万人民币可以在中国投资或消费

而贬值到8或更多的地步

就1万美元可以兑换8万甚至更多人民币,这时可以给更多人发工资,购买更多实物资产

反之

1元人民币要想换美元

可以是拿2元人民币换1美元,购买美国生产的物品

也可以8元人民币换1美元,购买美国生产的物品

美国量化宽松,配合中国的信贷和货币扩张阻止人民币升值,就是养羊的过程

中国的金融机构和美国投行再叫人民币贬值,用通过各国央行量化宽松的货币,来收购中国的资产

而这时美联储就一直上演永不加息的戏码,最后却猝不及防来个大加息,使很多人,辛苦做好的事业,以极低的价格贱卖

ps.中国的上层和西方的上层都在玩君主论http://www.constitution.org/mac/prince00.htm的那套东西

比如贬值会使很多人失业,这些人创造出一些物质财富最终积攒一些财富,就通过剪羊毛的方式让他们一无所有,他们只能再去创造物质财富,等待下一轮剪羊毛

但是第二次外出工作创造财富,究竟给谁干,却是个关键点,很重要的问题

比如贬值以后,明明是中国和外国一起联合剪羊毛,但贬值的过程,却是外国人在中国的配合下,在中国突然有了更多资金,可以雇佣更多人

给外国人干,和给中国人干,其实区别也不是很大

但很多人根本就没意识到这点

Fed QE China’s yuan devaluation Fed Raise Rates https://www.google.com.tw

外资 site://www.caogen.com https://www.google.com.tw

我回想起08年我去香港前后的真实心态,就是我刻意关注了香港的贫富差距,我走到很多香港的旧街区,去看了很多穷人生活的场景

然而我自己的审美,却决定,我不喜欢穷人生活的街区

我自己的审美,也决定了,我在香港消费不起任何物品

但是回来以后,我写了一些香港的购物心得的帖子,这时恶狗恶狼王菲在网上爆出,出轨的消息,恶狗恶狼王菲,还跟她出轨的情人,一起逛了北京的一个折扣店

我在北京也逛过这个折扣店,我回来后,连同香港的购物心得,把这些店都评价了一番

我对香港的普通的商场,以及北京的普通的商场,评价都不高

后来美联储和中国央行http://ytilauxes.blogspot.com/2016/06/blog-post_2.html就联手加息,打压我的气焰。他们认为我没有资格,要求过,符合我自己审美的生活

06年剪羊毛时,我在北京嚎啕大哭http://ytilauxes.blogspot.com/2016/08/freegate20168.html,对他人做道德判断价值判断,后来我外出购物,别人都在负成本甩卖各种物品,我也一边哭一边买

http://www.federalreserve.gov/newsevents/speech/yellen20160826a.htm 美联储网站的内容,同样的链接,瞬间就改变了内容,之前看到这个同样的链接,打开看,还有就业等的字样,后来再打开,就没有了

1美元可以兑换2元人民币

美国人或其他国家的人,把货币兑换成美元,拿到中国来,1万美元就有2万人民币可以在中国投资或消费

而贬值到8或更多的地步

就1万美元可以兑换8万甚至更多人民币,这时可以给更多人发工资,购买更多实物资产

反之

1元人民币要想换美元

可以是拿2元人民币换1美元,购买美国生产的物品

也可以8元人民币换1美元,购买美国生产的物品

美国量化宽松,配合中国的信贷和货币扩张阻止人民币升值,就是养羊的过程

中国的金融机构和美国投行再叫人民币贬值,用通过各国央行量化宽松的货币,来收购中国的资产

而这时美联储就一直上演永不加息的戏码,最后却猝不及防来个大加息,使很多人,辛苦做好的事业,以极低的价格贱卖

ps.中国的上层和西方的上层都在玩君主论http://www.constitution.org/mac/prince00.htm的那套东西

比如贬值会使很多人失业,这些人创造出一些物质财富最终积攒一些财富,就通过剪羊毛的方式让他们一无所有,他们只能再去创造物质财富,等待下一轮剪羊毛

但是第二次外出工作创造财富,究竟给谁干,却是个关键点,很重要的问题

比如贬值以后,明明是中国和外国一起联合剪羊毛,但贬值的过程,却是外国人在中国的配合下,在中国突然有了更多资金,可以雇佣更多人

给外国人干,和给中国人干,其实区别也不是很大

但很多人根本就没意识到这点

Fed QE China’s yuan devaluation Fed Raise Rates https://www.google.com.tw

外资 site://www.caogen.com https://www.google.com.tw

我回想起08年我去香港前后的真实心态,就是我刻意关注了香港的贫富差距,我走到很多香港的旧街区,去看了很多穷人生活的场景

然而我自己的审美,却决定,我不喜欢穷人生活的街区

我自己的审美,也决定了,我在香港消费不起任何物品

但是回来以后,我写了一些香港的购物心得的帖子,这时恶狗恶狼王菲在网上爆出,出轨的消息,恶狗恶狼王菲,还跟她出轨的情人,一起逛了北京的一个折扣店

我在北京也逛过这个折扣店,我回来后,连同香港的购物心得,把这些店都评价了一番

我对香港的普通的商场,以及北京的普通的商场,评价都不高

后来美联储和中国央行http://ytilauxes.blogspot.com/2016/06/blog-post_2.html就联手加息,打压我的气焰。他们认为我没有资格,要求过,符合我自己审美的生活

06年剪羊毛时,我在北京嚎啕大哭http://ytilauxes.blogspot.com/2016/08/freegate20168.html,对他人做道德判断价值判断,后来我外出购物,别人都在负成本甩卖各种物品,我也一边哭一边买

http://www.federalreserve.gov/newsevents/speech/yellen20160826a.htm 美联储网站的内容,同样的链接,瞬间就改变了内容,之前看到这个同样的链接,打开看,还有就业等的字样,后来再打开,就没有了

The Federal Reserve's Monetary Policy Toolkit: Past, Present, and Future

The Global Financial Crisis and Great Recession posed daunting new challenges for central banks around the world and spurred innovations in the design, implementation, and communication of monetary policy. With the U.S. economy now nearing the Federal Reserve's statutory goals of maximum employment and price stability, this conference provides a timely opportunity to consider how the lessons we learned are likely to influence the conduct of monetary policy in the future.

The theme of the conference, "Designing Resilient Monetary Policy Frameworks for the Future," encompasses many aspects of monetary policy, from the nitty-gritty details of implementing policy in financial markets to broader questions about how policy affects the economy. Within the operational realm, key choices include the selection of policy instruments, the specific markets in which the central bank participates, and the size and structure of the central bank's balance sheet. These topics are of great importance to the Federal Reserve. As noted in the minutes of last month's Federal Open Market Committee (FOMC) meeting, we are studying many issues related to policy implementation, research which ultimately will inform the FOMC's views on how to most effectively conduct monetary policy in the years ahead. I expect that the work discussed at this conference will make valuable contributions to the understanding of many of these important issues.

My focus today will be the policy tools that are needed to ensure that we have a resilient monetary policy framework. In particular, I will focus on whether our existing tools are adequate to respond to future economic downturns. As I will argue, one lesson from the crisis is that our pre-crisis toolkit was inadequate to address the range of economic circumstances that we faced. Looking ahead, we will likely need to retain many of the monetary policy tools that were developed to promote recovery from the crisis. In addition, policymakers inside and outside the Fed may wish at some point to consider additional options to secure a strong and resilient economy. But before I turn to these longer-run issues, I would like to offer a few remarks on the near-term outlook for the U.S. economy and the potential implications for monetary policy.

Current Economic Situation and Outlook

U.S. economic activity continues to expand, led by solid growth in household spending. But business investment remains soft and subdued foreign demand and the appreciation of the dollar since mid-2014 continue to restrain exports. While economic growth has not been rapid, it has been sufficient to generate further improvement in the labor market. Smoothing through the monthly ups and downs, job gains averaged 190,000 per month over the past three months. Although the unemployment rate has remained fairly steady this year, near 5 percent, broader measures of labor utilization have improved. Inflation has continued to run below the FOMC's objective of 2 percent, reflecting in part the transitory effects of earlier declines in energy and import prices.

U.S. economic activity continues to expand, led by solid growth in household spending. But business investment remains soft and subdued foreign demand and the appreciation of the dollar since mid-2014 continue to restrain exports. While economic growth has not been rapid, it has been sufficient to generate further improvement in the labor market. Smoothing through the monthly ups and downs, job gains averaged 190,000 per month over the past three months. Although the unemployment rate has remained fairly steady this year, near 5 percent, broader measures of labor utilization have improved. Inflation has continued to run below the FOMC's objective of 2 percent, reflecting in part the transitory effects of earlier declines in energy and import prices.

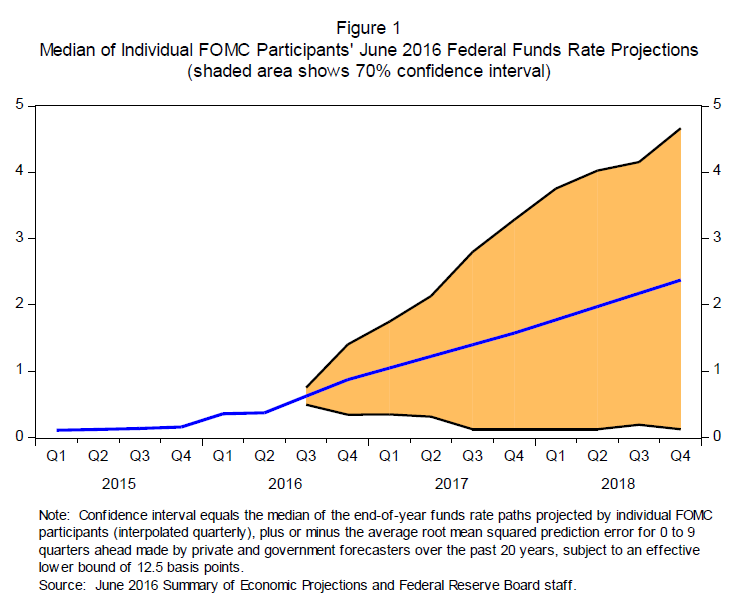

Looking ahead, the FOMC expects moderate growth in real gross domestic product (GDP), additional strengthening in the labor market, and inflation rising to 2 percent over the next few years. Based on this economic outlook, the FOMC continues to anticipate that gradual increases in the federal funds rate will be appropriate over time to achieve and sustain employment and inflation near our statutory objectives. Indeed, in light of the continued solid performance of the labor market and our outlook for economic activity and inflation, I believe the case for an increase in the federal funds rate has strengthened in recent months. Of course, our decisions always depend on the degree to which incoming data continues to confirm the Committee's outlook.

And, as ever, the economic outlook is uncertain, and so monetary policy is not on a preset course. Our ability to predict how the federal funds rate will evolve over time is quite limited because monetary policy will need to respond to whatever disturbances may buffet the economy. In addition, the level of short-term interest rates consistent with the dual mandate varies over time in response to shifts in underlying economic conditions that are often evident only in hindsight. For these reasons, the range of reasonably likely outcomes for the federal funds rate is quite wide--a point illustrated by figure 1 in your handout. The line in the center is the median path for the federal funds rate based on the FOMC's Summary of Economic Projections in June.1 The shaded region, which is based on the historical accuracy of private and government forecasters, shows a 70 percent probability that the federal funds rate will be between 0 and 3-1/4 percent at the end of next year and between 0 and 4-1/2 percent at the end of 2018.2 The reason for the wide range is that the economy is frequently buffeted by shocks and thus rarely evolves as predicted. When shocks occur and the economic outlook changes, monetary policy needs to adjust. What we do know, however, is that we want a policy toolkit that will allow us to respond to a wide range of possible conditions.

The Pre-Crisis Toolkit

Prior to the financial crisis, the Federal Reserve's monetary policy toolkit was simple but effective in the circumstances that then prevailed. Our main tool consisted of open market operations to manage the amount of reserve balances available to the banking sector.3 These operations, in turn, influenced the interest rate in the federal funds market, where banks experiencing reserve shortfalls could borrow from banks with excess reserves. Before the onset of the crisis, the volume of reserves was generally small--only about $45 billion or so.4 Thus, even small open market operations could have a significant effect on the federal funds rate. Changes in the federal funds rate would then be transmitted to other short-term interest rates, affecting longer-term interest rates and overall financial conditions and hence inflation and economic activity. This simple, light-touch system allowed the Federal Reserve to operate with a relatively small balance sheet--less than $1 trillion before the crisis--the size of which was largely determined by the need to supply enough U.S. currency to meet demand.5

Prior to the financial crisis, the Federal Reserve's monetary policy toolkit was simple but effective in the circumstances that then prevailed. Our main tool consisted of open market operations to manage the amount of reserve balances available to the banking sector.3 These operations, in turn, influenced the interest rate in the federal funds market, where banks experiencing reserve shortfalls could borrow from banks with excess reserves. Before the onset of the crisis, the volume of reserves was generally small--only about $45 billion or so.4 Thus, even small open market operations could have a significant effect on the federal funds rate. Changes in the federal funds rate would then be transmitted to other short-term interest rates, affecting longer-term interest rates and overall financial conditions and hence inflation and economic activity. This simple, light-touch system allowed the Federal Reserve to operate with a relatively small balance sheet--less than $1 trillion before the crisis--the size of which was largely determined by the need to supply enough U.S. currency to meet demand.5

The global financial crisis revealed two main shortcomings of this simple toolkit. The first was an inability to control the federal funds rate once reserves were no longer relatively scarce. Starting in late 2007, faced with acute financial market distress, the Federal Reserve created programs to keep credit flowing to households and businesses.6 The loans extended under those programs helped stabilize the financial system. But the additional reserves created by these programs, if left unchecked, would have pushed down the federal funds rate, driving it well below the FOMC's target. To prevent such an outcome, the Federal Reserve took several steps to offset (or sterilize) the effect of its liquidity and credit operations on reserves.7 By the fall of 2008, however, the reserve effects of our liquidity and credit programs threatened to become too large to sterilize via asset sales and other existing tools. Without sufficient sterilization capacity, the quantity of reserves increased to a point that the Federal Reserve had difficulty maintaining effective control over the federal funds rate.

Of course, by the end of 2008, stabilizing the federal funds rate at a level materially above zero was not an immediate concern because the economy clearly needed very low short-term interest rates. Faced with a steep rise in unemployment and declining inflation, the FOMC lowered its target for the federal funds rate to near zero, a reduction of roughly 5 percentage points over the previous year and a half. Nonetheless, a variety of policy benchmarks would, at least in hindsight, have called for pushing the federal funds rate well below zero during the economic downturn.8 That doing so was impossible highlights the second serious limitation of our pre-crisis policy toolkit: its inability to generate substantially more accommodation than could be provided by a near-zero federal funds rate.

Our Expanded Toolkit

To address the challenges posed by the financial crisis and the subsequent severe recession and slow recovery, the Federal Reserve significantly expanded its monetary policy toolkit. In 2006, the Congress had approved plans to allow the Fed, beginning in 2011, to pay interest on banks' reserve balances.9 In the fall of 2008, the Congress moved up the effective date of this authority to October 2008. That authority was essential. Paying interest on reserve balances enables the Fed to break the strong link between the quantity of reserves and the level of the federal funds rate and, in turn, allows the Federal Reserve to control short-term interest rates when reserves are plentiful. In particular, once economic conditions warrant a higher level for market interest rates, the Federal Reserve could raise the interest rate paid on excess reserves--the IOER rate. A higher IOER rate encourages banks to raise the interest rates they charge, putting upward pressure on market interest rates regardless of the level of reserves in the banking sector.

To address the challenges posed by the financial crisis and the subsequent severe recession and slow recovery, the Federal Reserve significantly expanded its monetary policy toolkit. In 2006, the Congress had approved plans to allow the Fed, beginning in 2011, to pay interest on banks' reserve balances.9 In the fall of 2008, the Congress moved up the effective date of this authority to October 2008. That authority was essential. Paying interest on reserve balances enables the Fed to break the strong link between the quantity of reserves and the level of the federal funds rate and, in turn, allows the Federal Reserve to control short-term interest rates when reserves are plentiful. In particular, once economic conditions warrant a higher level for market interest rates, the Federal Reserve could raise the interest rate paid on excess reserves--the IOER rate. A higher IOER rate encourages banks to raise the interest rates they charge, putting upward pressure on market interest rates regardless of the level of reserves in the banking sector.

While adjusting the IOER rate is an effective way to move market interest rates when reserves are plentiful, federal funds have generally traded below this rate. This relative softness of the federal funds rate reflects, in part, the fact that only depository institutions can earn the IOER rate. To put a more effective floor under short-term interest rates, the Federal Reserve created supplementary tools to be used as needed. For instance, the overnight reverse repurchase agreement (ON RRP) facility is available to a variety of counterparties, including eligible money market funds, government-sponsored enterprises, broker-dealers, and depository institutions. Through it, eligible counterparties may invest funds overnight with the Federal Reserve at a rate determined by the FOMC. Similar to the payment of IOER, the ON RRP facility discourages participating institutions from lending at a rate substantially below that offered by the Fed.10

Our current toolkit proved effective last December. In an environment of superabundant reserves, the FOMC raised the effective federal funds rate--that is, the weighted average rate on federal funds transactions among participants in that market--by the desired amount, and we have since maintained the federal funds rate in its target range.

Two other major additions to the Fed's toolkit were large-scale asset purchases and increasingly explicit forward guidance.11 Both were used to provide additional monetary policy accommodation after short-term interest rates fell close to zero. Our purchases of Treasury and mortgage-related securities in the open market pushed down longer-term borrowing rates for millions of American families and businesses. Extended forward rate guidance--announcing that we intended to keep short-term interest rates lower for longer than might have otherwise been expected--also put significant downward pressure on longer-term borrowing rates, as did guidance regarding the size and scope of our asset purchases.

In light of the slowness of the economic recovery, some have questioned the effectiveness of asset purchases and extended forward rate guidance. But this criticism fails to consider the unusual headwinds the economy faced after the crisis. Those headwinds included substantial household and business deleveraging, unfavorable demand shocks from abroad, a period of contractionary fiscal policy, and unusually tight credit, especially for housing. Studies have found that our asset purchases and extended forward rate guidance put appreciable downward pressure on long-term interest rates and, as a result, helped spur growth in demand for goods and services, lower the unemployment rate, and prevent inflation from falling further below our 2 percent objective.12

Two of the Fed's most important new tools--our authority to pay interest on excess reserves and our asset purchases--interacted importantly. Without IOER authority, the Federal Reserve would have been reluctant to buy as many assets as it did because of the longer-run implications for controlling the stance of monetary policy. While we were buying assets aggressively to help bring the U.S. economy out of a severe recession, we also had to keep in mind whether and how we would be able to remove monetary policy accommodation when appropriate. That issue was particularly relevant because we fund our asset purchases through the creation of reserves, and those additional reserves would have made it ever more difficult for the pre-crisis toolkit to raise short-term interest rates when needed.

The FOMC considered removing accommodation by first reducing our asset holdings (including through asset sales) and raising the federal funds rate only after our balance sheet had contracted substantially. But we decided against this approach because our ability to predict the effects of changes in the balance sheet on the economy is less than that associated with changes in the federal funds rate. Excessive inflationary pressures could arise if assets were sold too slowly. Conversely, financial markets and the economy could potentially be destabilized if assets were sold too aggressively. Indeed, the so-called taper tantrum of 2013 illustrates the difficulty of predicting financial market reactions to announcements about the balance sheet. Given the uncertainty and potential costs associated with large-scale asset sales, the FOMC instead decided to begin removing monetary policy accommodation primarily by adjusting short-term interest rates rather than by actively managing its asset holdings.13 That strategy--raising short-term interest rates once the recovery was sufficiently advanced while maintaining a relatively large balance sheet and plentiful bank reserves--depended on our ability to pay interest on excess reserves.

Where Do We Go from Here?

What does the future hold for the Fed's toolkit? For starters, our ability to use interest on reserves is likely to play a key role for years to come. In part, this reflects the outlook for our balance sheet over the next few years. As the FOMC has noted in its recent statements, at some point after the process of raising the federal funds rate is well under way, we will cease or phase out reinvesting repayments of principal from our securities holdings. Once we stop reinvestment, it should take several years for our asset holdings--and the bank reserves used to finance them--to passively decline to a more normal level. But even after the volume of reserves falls substantially, IOER will still be important as a contingency tool, because we may need to purchase assets during future recessions to supplement conventional interest rate reductions.14 Forecasts now show the federal funds rate settling at about 3 percent in the longer run.15 In contrast, the federal funds rate averaged more than 7 percent between 1965 and 2000. Thus, we expect to have less scope for interest rate cuts than we have had historically.

What does the future hold for the Fed's toolkit? For starters, our ability to use interest on reserves is likely to play a key role for years to come. In part, this reflects the outlook for our balance sheet over the next few years. As the FOMC has noted in its recent statements, at some point after the process of raising the federal funds rate is well under way, we will cease or phase out reinvesting repayments of principal from our securities holdings. Once we stop reinvestment, it should take several years for our asset holdings--and the bank reserves used to finance them--to passively decline to a more normal level. But even after the volume of reserves falls substantially, IOER will still be important as a contingency tool, because we may need to purchase assets during future recessions to supplement conventional interest rate reductions.14 Forecasts now show the federal funds rate settling at about 3 percent in the longer run.15 In contrast, the federal funds rate averaged more than 7 percent between 1965 and 2000. Thus, we expect to have less scope for interest rate cuts than we have had historically.

In part, current expectations for a low future federal funds rate reflect the FOMC's success in stabilizing inflation at around 2 percent--a rate much lower than rates that prevailed during the 1970s and 1980s. Another key factor is the marked decline over the past decade, both here and abroad, in the long-run neutral real rate of interest--that is, the inflation-adjusted short-term interest rate consistent with keeping output at its potential on average over time.16 Several developments could have contributed to this apparent decline, including slower growth in the working-age populations of many countries, smaller productivity gains in the advanced economies, a decreased propensity to spend in the wake of the financial crises around the world since the late 1990s, and perhaps a paucity of attractive capital projects worldwide.17 Although these factors may help explain why bond yields have fallen to such low levels here and abroad, our understanding of the forces driving long-run trends in interest rates is nevertheless limited, and thus all predictions in this area are highly uncertain.18

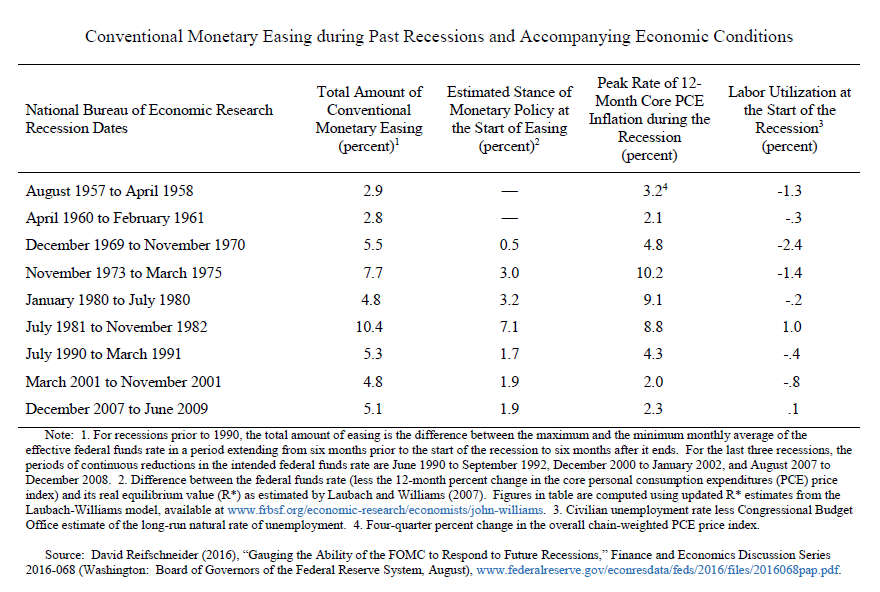

Would an average federal funds rate of about 3 percent impair the Fed's ability to fight recessions? Based on the FOMC's behavior in past recessions, one might think that such a low interest rate could substantially impair policy effectiveness. As shown in the first column of the table in the handout, during the past nine recessions, the FOMC cut the federal funds rate by amounts ranging from about 3 percentage points to more than 10 percentage points. On average, the FOMC reduced rates by about 5-1/2 percentage points, which seems to suggest that the FOMC would face a shortfall of about 2-1/2 percentage points for dealing with an average-sized recession. But this simple comparison exaggerates the limitations on policy created by the zero lower bound. As shown in the second column, the federal funds rate at the start of the past seven recessions was appreciably above the level consistent with the economy operating at potential in the longer run. In most cases, this tighter-than-normal stance of policy before the recession appears to have reflected some combination of initially higher-than-normal labor utilization and elevated inflation pressures. As a result, a large portion of the rate cuts that subsequently occurred during these recessions represented the undoing of the earlier tight stance of monetary policy. Of course, this situation could occur again in the future. But if it did, the federal funds rate at the onset of the recession would be well above its normal level, and the FOMC would be able to cut short-term interest rates by substantially more than 3 percentage points.

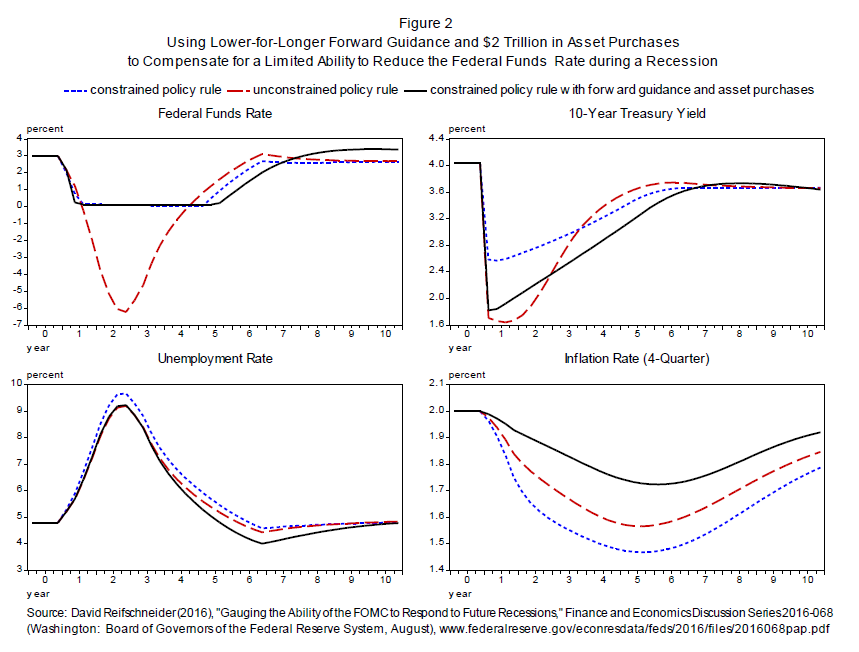

A recent paper takes a different approach to assessing the FOMC's ability to respond to future recessions by using simulations of the FRB/US model.19 This analysis begins by asking how the economy would respond to a set of highly adverse shocks if policymakers followed a fairly aggressive policy rule, hypothetically assuming that they can cut the federal funds rate without limit.20 It then imposes the zero lower bound and asks whether some combination of forward guidance and asset purchases would be sufficient to generate economic conditions at least as good as those that occur under the hypothetical unconstrained policy. In general, the study concludes that, even if the average level of the federal funds rate in the future is only 3 percent, these new tools should be sufficient unless the recession were to be unusually severe and persistent.

Figure 2 in your handout illustrates this point. It shows simulated paths for interest rates, the unemployment rate, and inflation under three different monetary policy responses--the aggressive rule in the absence of the zero lower bound constraint, the constrained aggressive rule, and the constrained aggressive rule combined with $2 trillion in asset purchases and guidance that the federal funds rate will depart from the rule by staying lower for longer.21 As the blue dashed line shows, the federal funds rate would fall far below zero if policy were unconstrained, thereby causing long-term interest rates to fall sharply. But despite the lower bound, asset purchases and forward guidance can push long-term interest rates even lower on average than in the unconstrained case (especially when adjusted for inflation) by reducing term premiums and increasing the downward pressure on the expected average value of future short-term interest rates. Thus, the use of such tools could result in even better outcomes for unemployment and inflation on average.

Of course, this analysis could be too optimistic. For one, the FRB/US simulations may overstate the effectiveness of forward guidance and asset purchases, particularly in an environment where long-term interest rates are also likely to be unusually low.22 In addition, policymakers could have less ability to cut short-term interest rates in the future than the simulations assume. By some calculations, the real neutral rate is currently close to zero, and it could remain at this low level if we were to continue to see slow productivity growth and high global saving.23 If so, then the average level of the nominal federal funds rate down the road might turn out to be only 2 percent, implying that asset purchases and forward guidance might have to be pushed to extremes to compensate.24 Moreover, relying too heavily on these nontraditional tools could have unintended consequences. For example, if future policymakers responded to a severe recession by announcing their intention to keep the federal funds rate near zero for a very long time after the economy had substantially recovered and followed through on that guidance, then they might inadvertently encourage excessive risk-taking and so undermine financial stability.

Finally, the simulation analysis certainly overstates the FOMC's current ability to respond to a recession, given that there is little scope to cut the federal funds rate at the moment. But that does not mean that the Federal Reserve would be unable to provide appreciable accommodation should the ongoing expansion falter in the near term. In addition to taking the federal funds rate back down to nearly zero, the FOMC could resume asset purchases and announce its intention to keep the federal funds rate at this level until conditions had improved markedly--although with long-term interest rates already quite low, the net stimulus that would result might be somewhat reduced.

Despite these caveats, I expect that forward guidance and asset purchases will remain important components of the Fed's policy toolkit. In addition, it is critical that the Federal Reserve and other supervisory agencies continue to do all they can to ensure a strong and resilient financial system. That said, these tools are not a panacea, and future policymakers could find that they are not adequate to deal with deep and prolonged economic downturns. For these reasons, policymakers and society more broadly may want to explore additional options for helping to foster a strong economy.

On the monetary policy side, future policymakers might choose to consider some additional tools that have been employed by other central banks, though adding them to our toolkit would require a very careful weighing of costs and benefits and, in some cases, could require legislation. For example, future policymakers may wish to explore the possibility of purchasing a broader range of assets. Beyond that, some observers have suggested raising the FOMC's 2 percent inflation objective or implementing policy through alternative monetary policy frameworks, such as price-level or nominal GDP targeting. I should stress, however, that the FOMC is not actively considering these additional tools and policy frameworks, although they are important subjects for research.

Beyond monetary policy, fiscal policy has traditionally played an important role in dealing with severe economic downturns. A wide range of possible fiscal policy tools and approaches could enhance the cyclical stability of the economy.25 For example, steps could be taken to increase the effectiveness of the automatic stabilizers, and some economists have proposed that greater fiscal support could be usefully provided to state and local governments during recessions. As always, it would be important to ensure that any fiscal policy changes did not compromise long-run fiscal sustainability.

Finally, and most ambitiously, as a society we should explore ways to raise productivity growth. Stronger productivity growth would tend to raise the average level of interest rates and therefore would provide the Federal Reserve with greater scope to ease monetary policy in the event of a recession. But more importantly, stronger productivity growth would enhance Americans' living standards. Though outside the narrow field of monetary policy, many possibilities in this arena are worth considering, including improving our educational system and investing more in worker training; promoting capital investment and research spending, both private and public; and looking for ways to reduce regulatory burdens while protecting important economic, financial, and social goals.

Conclusion

Although fiscal policies and structural reforms can play an important role in strengthening the U.S. economy, my primary message today is that I expect monetary policy will continue to play a vital part in promoting a stable and healthy economy. New policy tools, which helped the Federal Reserve respond to the financial crisis and Great Recession, are likely to remain useful in dealing with future downturns. Additional tools may be needed and will be the subject of research and debate. But even if average interest rates remain lower than in the past, I believe that monetary policy will, under most conditions, be able to respond effectively.

Although fiscal policies and structural reforms can play an important role in strengthening the U.S. economy, my primary message today is that I expect monetary policy will continue to play a vital part in promoting a stable and healthy economy. New policy tools, which helped the Federal Reserve respond to the financial crisis and Great Recession, are likely to remain useful in dealing with future downturns. Additional tools may be needed and will be the subject of research and debate. But even if average interest rates remain lower than in the past, I believe that monetary policy will, under most conditions, be able to respond effectively.

1. The June 2016 Summary of Economic Projections (SEP) is an addendum to the minutes of the June 2016 FOMC meeting and is available on the Board's website atwww.federalreserve.gov/monetarypolicy/files/fomcminutes20160615.pdf. Return to text

2. The confidence interval equals (subject to a lower bound of 12.5 basis points) the median SEP path for the federal funds rate plus or minus average root mean squared prediction errors (RMSPEs) of the three-month Treasury bill rate, for horizons from zero to nine quarters ahead, based on forecast errors made over the past 20 years. Average RMSPEs are calculated as the mean of the RMSPEs of the following forecasters, subject to availability for the horizon in question: the Federal Reserve Board staff (Greenbook/Tealbook), the Administration, the Congressional Budget Office, the Blue Chip consensus forecast, and the Survey of Professional Forecasters. Differences in predictive accuracy among these forecasters are not statistically significant. For more information on the general methodology used to construct confidence intervals using historical forecasting errors, see David Reifschneider and Peter Tulip (2007), "Gauging the Uncertainty of the Economic Outlook from Historical Forecasting Errors (PDF)," Finance and Economics Discussion Series 2007-60 (Washington: Board of Governors of the Federal Reserve System, November). Return to text

3. Open market operations at the time were primarily repurchase agreements based on Treasury securities, with primary dealers as counterparties. Return to text

4. Reserves of depository institutions include vault cash and balances maintained with Federal Reserve Banks. Excess reserves are the reserves held over and above required reserves. See the Board's webpage "Reserve Requirements" at www.federalreserve.gov/monetarypolicy/reservereq.htm. Return to text

5. Prior to the financial crisis, the size of the Fed's balance sheet was about $900 billion. Assets consisted almost entirely of Treasury securities. Liabilities included currency held by the public and a relatively small volume of reserve balances. For more on the Fed's balance sheet, seewww.federalreserve.gov/monetarypolicy/bst_fedsbalancesheet.htm. Return to text

6. For information on the Federal Reserve's credit and liquidity programs that were implemented in response to the financial crisis, see www.federalreserve.gov/monetarypolicy/bst_crisisresponse.htm on the Board's website. Return to text

7. Reserves were initially taken out of the banking system by not reinvesting principal payments from maturing securities and later by selling portions of securities holdings. In September 2008, the Department of the Treasury announced the temporary Supplementary Financing Program, in which the proceeds of a series of Treasury bill auctions, separate from Treasury's routine borrowing, were maintained in an account at the Federal Reserve Bank of New York. The funds in this account served to drain reserves from the banking system. Return to text

8. Consider the following policy rule: R(t) = R* + p(t) + 0.5[p(t)-p*]-2.0[U(t)-U*], where R is the federal funds rate, R* is the longer-run normal value of the federal funds rate adjusted for inflation, p is the four-quarter moving average of core PCE inflation, p* is the FOMC's target for inflation (2 percent), U is the unemployment rate, and U* is the longer-run normal rate of unemployment. Based on the medians of FOMC participants' latest longer-run projections, R* is approximately 1 percent and U* is about 4.8 percent. Accordingly, with the unemployment rate climbing to 10 percent and core PCE inflation falling to 1 percent in 2009, this rule would have prescribed lowering the federal funds rate to minus 9 percent at the depths of the recession. In contrast, the standard Taylor rule, which is half as responsive to movements in resource utilization, would have prescribed lowering the federal funds rate to minus 3-3/4 percent using the same estimates for R* and U*. The more aggressive rule does a reasonably good job of accounting for movements in the federal funds rate in the decade prior to its falling to its effective lower bound in late 2008, see David Reifschneider (2016), "Gauging the Ability of the FOMC to Respond to Future Recessions (PDF)," Finance and Economics Discussion Series 2016-068 (Washington: Board of Governors of the Federal Reserve System, August). For more information on the standard Taylor rule, see John B. Taylor (1993), "Discretion versus Policy Rules in Practice," Carnegie-Rochester Conference Series on Public Policy, vol. 39 (December), pp. 195-214.Return to text

9. Paying interest on reserves is a tool commonly used by central banks, including the Bank of England, the Bank of Japan, and the European Central Bank. Return to text

10. Other tools that could help strengthen the floor under short-term interest rates but are not currently in use include the Term Deposit Facility and term reverse repurchase agreements. Return to text

11. Prior to the crisis, the Fed occasionally used forward guidance pertaining to the likely future path of interest rates, but that guidance was usually confined to a relatively short time frame. Return to text

12. See, for instance, Joseph Gagnon, Matthew Raskin, Julie Remache, and Brian Sack (2011), "The Financial Market Effects of the Federal Reserve's Large-Scale Asset Purchases,"  International Journal of Central Banking, vol. 7 (March), pp. 3-43; and Stefania D'Amico, William English, David López-Salido, and Edward Nelson (2012), "The Federal Reserve's Large-Scale Asset Purchase Programmes: Rationale and Effects," Economic Journal, vol. 122 (November), pp. F415-46. Moreover, the Federal Reserve's forward guidance and asset purchase policies have been estimated to have helped lower unemployment and boost inflation; see Eric M. Engen, Thomas Laubach, and David Reifschneider (2015), "The Macroeconomic Effects of the Federal Reserve's Unconventional Monetary Policies," Finance and Economics Discussion Series 2015-005 (Washington: Board of Governors of the Federal Reserve System, January). Return to text

International Journal of Central Banking, vol. 7 (March), pp. 3-43; and Stefania D'Amico, William English, David López-Salido, and Edward Nelson (2012), "The Federal Reserve's Large-Scale Asset Purchase Programmes: Rationale and Effects," Economic Journal, vol. 122 (November), pp. F415-46. Moreover, the Federal Reserve's forward guidance and asset purchase policies have been estimated to have helped lower unemployment and boost inflation; see Eric M. Engen, Thomas Laubach, and David Reifschneider (2015), "The Macroeconomic Effects of the Federal Reserve's Unconventional Monetary Policies," Finance and Economics Discussion Series 2015-005 (Washington: Board of Governors of the Federal Reserve System, January). Return to text

International Journal of Central Banking, vol. 7 (March), pp. 3-43; and Stefania D'Amico, William English, David López-Salido, and Edward Nelson (2012), "The Federal Reserve's Large-Scale Asset Purchase Programmes: Rationale and Effects," Economic Journal, vol. 122 (November), pp. F415-46. Moreover, the Federal Reserve's forward guidance and asset purchase policies have been estimated to have helped lower unemployment and boost inflation; see Eric M. Engen, Thomas Laubach, and David Reifschneider (2015), "The Macroeconomic Effects of the Federal Reserve's Unconventional Monetary Policies," Finance and Economics Discussion Series 2015-005 (Washington: Board of Governors of the Federal Reserve System, January). Return to text13. The FOMC's "Policy Normalization Principles and Plans" call for reducing the Federal Reserve's securities holdings in a "gradual and predictable manner primarily by ceasing to reinvest repayments of principal on securities held in the [System Open Market Account]" (Board of Governors of the Federal Reserve System (2014), "Federal Reserve Issues FOMC Statement on Policy Normalization Principles and Plans," press release, September 17, second bullet). Consistent with those plans, the Federal Open Market Committee anticipates that it will maintain its current reinvestment strategy "until normalization of the level of the federal funds rate is well under way" (for instance, see Board of Governors of the Federal Reserve System (2015), "Federal Reserve Issues FOMC Statement," press release, December 16, paragraph 5. Return to text

14. If the FOMC were to again increase the size of the balance sheet markedly in response to a future recession, then the ability to pay interest on reserves could be critical during the subsequent recovery period to help control short-term interest rates while the balance sheet remains elevated. Beyond this motivation for retaining IOER, the ability to pay interest on reserves could also be important to the operation of any special liquidity and credit facilities that might be created to deal with systemic disruptions to the financial system during a future emergency. In particular, such facilities could significantly expand the supply of reserves, which would be problematic if the FOMC wished to keep short-term interest rates from falling to zero. Return to text

15. In the Blue Chip Financial Indicators survey released on June 1, 2016, the consensus forecast for the longer-run level of the federal funds rate was 3.2 percent. FOMC participants in June 2016 generally anticipated a slightly lower longer-run level, in that the median of their individual forecasts was 3 percent (see table 1 of the June 2016 SEP, available at www.federalreserve.gov/monetarypolicy/fomcminutes20160615ep.htm). The latest long-run forecast from the Administration (www.whitehouse.gov/sites/default/files/omb/budget/fy2016/assets/16msr.pdf) is also close to 3 percent, as was the projection made by the Congressional Budget Office earlier in the year (seewww.cbo.gov/about/products/budget_economic_data). Return to text

16. Updated estimates from the model developed by Laubach and Williams (2003) indicate that the real long-run neutral or "equilibrium" short-term interest rate in the United States is currently about 2-1/2 percentage points lower than it was on average in the 1980s and 1990s (see Thomas Laubach and John C. Williams (2003), "Measuring the Natural Rate of Interest," Review of Economics and Statistics, vol. 85 (November), pp. 1063-70; updated estimates are available at www.frbsf.org/economic-research/economists/john-williams/Laubach_Williams_updated_estimates.xlsx.) In addition, Holston, Laubach, and Williams (2016) find significant but somewhat smaller declines in equilibrium rates for the euro area, Canada, and the United Kingdom (see Kathryn Holston, Thomas Laubach, and John C. Williams (2016), "Measuring the Natural Rate of Interest: International Trends and Determinants," Working Paper 2016-11 (San Francisco: Federal Reserve Bank of San Francisco, June), www.frbsf.org/economic-research/files/wp2016-11.pdf). Return to text